by

Cliff Jamieson

,

Canadian Grains Analyst

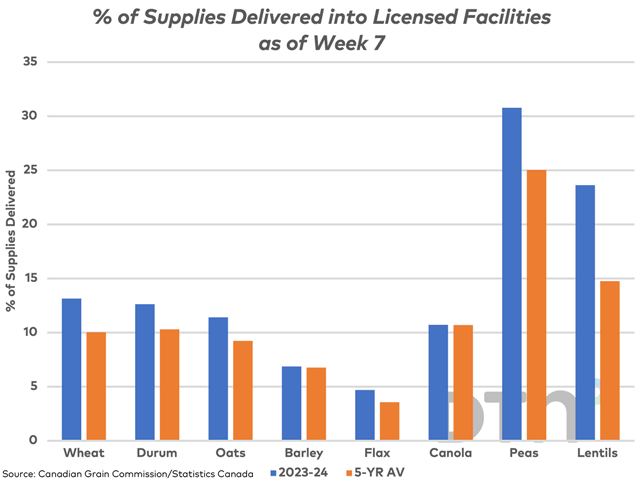

The Canadian Grain Commission has reported large weekly shipments of wheat from licensed facilities in two of the past three weeks. Cumulative shipments are higher than average, while ahead of the pace needed to reach the current AAFC forecast.