by

Cliff Jamieson

,

Canadian Grains Analyst

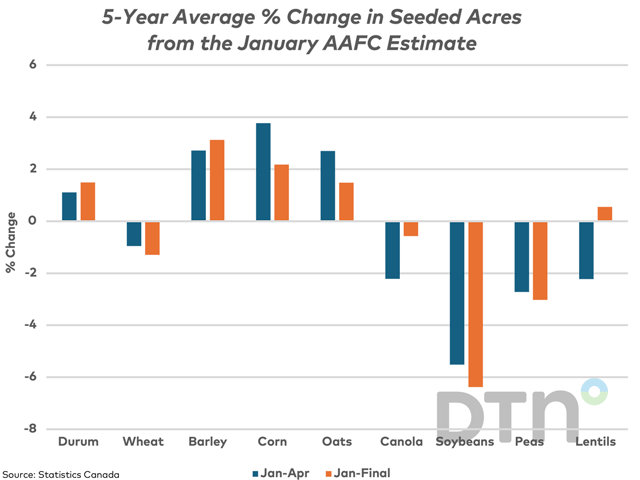

AAFC will soon release its initial forecasts for principal field crops for 2024-25. This study looks at the percent change in Statistics Canada's estimated seeded acres from this initial estimate.