by

Cliff Jamieson

,

Canadian Grains Analyst

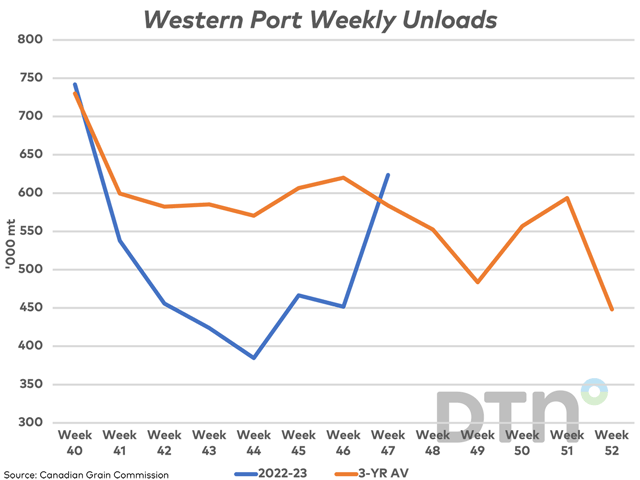

There has been a late crop-year increase seen in demand for cars for loading as well as terminal unloads, seen largely in movement of wheat, durum and canola.