by

Cliff Jamieson

,

Canadian Grains Analyst

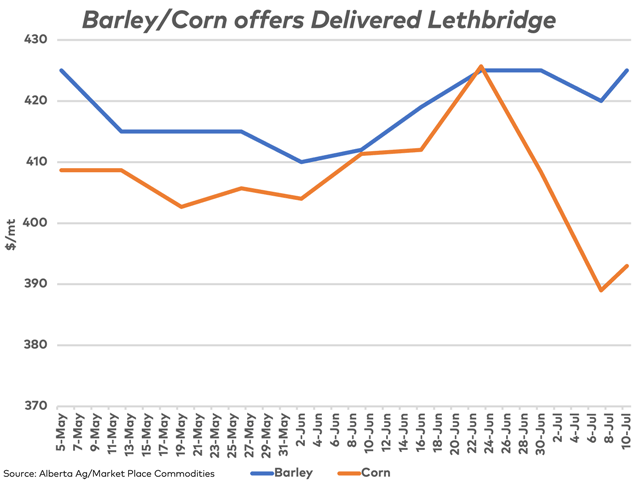

China has penalized Australia with an 80.5% anti-dumping tariff since 2020, which will come to an end on August 5. This will have implications for Canada's barley trade.