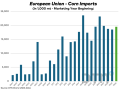

With corn production estimates in Europe falling and import projections rising, the situation is very likely to have a meaningful impact on North American feed grain markets and needs to be...

It will be a busy week for market numbers, with the DTN Digital Yield Tour estimates on corn and soybean yields, a WASDE report on Wednesday, and...

Blogger Tiffany Dowell Lashmet says deals generally should be settled in writing, but some handshake deals turn out to be winners for both parties.

Mitch Miller has joined the DTN team as the DTN Contributing Canadian Grains Analyst following a long career in the grain and oilseed sector in south-central Manitoba, Canada. He jokes that he has been a primary producer for almost 40 years by necessity but a market analyst and strategist throughout that by passion.

A bachelor's degree in ag economics from the University of Manitoba initiated a lifelong focus on all things management and marketing. Although the decision was made to downsize the farm significantly in 2019, he proudly claims to still have enough acres to seed and cows to feed to remain grounded.

Too young to quit being productive, he hopes to share some of his experience and insight with readers to help with one of the most challenging tasks on the farm -- marketing the production successfully. A six-year span as a commodity broker and a lifelong career involved in the cash market should provide a unique balance from which to draw.

In an attempt to be transparent, he explains his approach to market analysis. Looking for clues from fundamental analysis, technical analysis and from the market participants themselves through the Commitment of Trader reports, a theory on price direction is developed. The more clues supporting the theory, the more confidence in it. That in turn influences the development of a successful marketing strategy. Through this role, he hopes to be able to share those clues as they are identified on an ongoing basis.

With corn production estimates in Europe falling and import projections rising, the situation is very likely to have a meaningful impact on North American feed grain markets and needs to be...

With Statistics Canada's June seeded area forecast and in-crop yield estimates now available, AAFC updated its demand and ending stocks projections as well with a few interesting outcomes.

With corn production estimates in Europe falling and import projections rising, the situation is very likely to have a meaningful impact on North American feed grain markets and needs to be...

With Statistics Canada's June seeded area forecast and in-crop yield estimates now available, AAFC updated its demand and ending stocks projections as well with a few interesting outcomes.

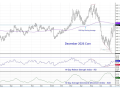

Technical analysis is an important part of the toolbox. The December corn chart provides numerous examples to demonstrate various formations.

Technical analysis is an important part of the toolbox. The December corn chart provides numerous examples to demonstrate various formations.

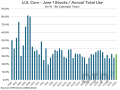

The current bounce in corn prices reminds us that stocks should always be compared to total use, which changes the picture significantly.

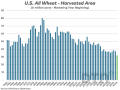

The greatest surprise in seeded area reports from both sides of the border Tuesday was the miss in total wheat area, with that likely to provide good price support for the coming year.

With the corn production cycle in Europe closely matching that in North America, timing couldn't be much worse for the ongoing drought and related heat wave. Increased corn imports will be hard to avoid.

With soybean oil used in biofuel production expected to soar in 2026-27, there is no room for exports to be anything more than token amounts for the foreseeable future.

Amid drought, El Nino and crop input concerns, ABARES gave a pessimistic June outlook for the 2026-27 winter crop potential.

The soybean/corn price ratio continues to support a shift in area from corn to soybean planting as the season wraps up, backing ideas that corn acres are likely to decline further in the June report.

The soybean/corn price ratio continues to support a shift in area from corn to soybean planting as the season wraps up, backing ideas that corn acres are likely to decline further in the June report.

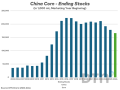

Should China fulfill its commitment to purchase additional U.S. ag products as announced following Trump's visit, corn would certainly be a sensible option.

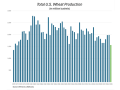

Nothing cures low prices like low prices. Producers had enough of poor returns from wheat and reduced area, then Mother Nature helped cut production even further.