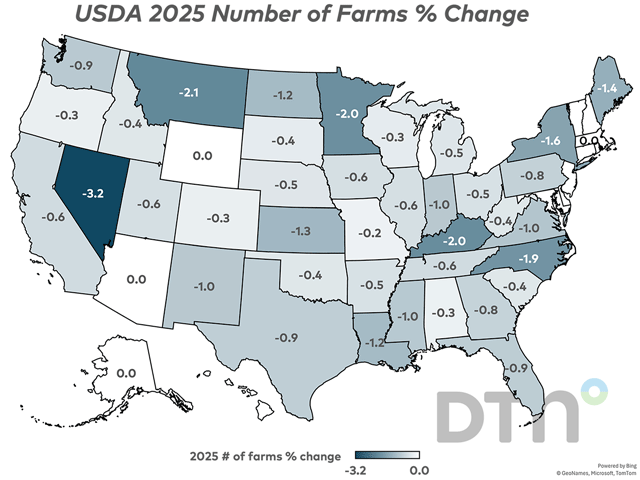

Canada Markets

Wheat's Best Hope for a Rally May Rest With Corn

Ever since the blowoff top that accompanied the Russian invasion of Ukraine, wheat markets have been the whipping boy for traders. It doesn't matter what is going on, wheat gets sold on any rally -- with that working well for three years now. With July Kansas wheat putting in a new contract low Thursday (and Chicago not far behind), the few remaining bulls are desperately looking for something that might provide relief. As seen in the accompanying chart, corn may hold the key.

Before moving on, it's worth a brief recap of the damage done during the early days of the Russian invasion -- financially and psychologically -- to traders in the wheat markets. From Feb. 3 to March 8, nearby Chicago wheat rallied $5.45/bushel (from $7.40 to $12.85), often with limit moves along the way. Those caught on the short side at the time suffered serious financial damage. Trader confidence in the liquidity of the market (ability to enter and exit as desired) took just as severe of a hit. Then bulls were slaughtered (pardon the pun) when the price fell $4.99/bushel (from May 17 to July 6), while the early days of the war raged on. It took well over a year for open interest to return to pre-invasion levels. And ever since, the traders that regained the most confidence in the market are using it to successfully sell into any rally. So far anyway.

The managed money trader group has been the most consistently aggressive with their selling -- net short 143,811 contracts or 719 million bushels (mb) between Chicago and Kansas City wheat as of April 15. To put that into perspective, the combined ending stocks for the two types of wheat for 2024-25 is expected to be 524 mb. A rapid short-covering event by this group would be expected to have a serious impact on prices and looking for a potential trigger is important.

Even though there are many bullish factors the market has chosen to ignore, one of the more likely triggers could be the narrow premium wheat has to the price of corn. As you can see from the accompanying chart, when corn prices come within $.50/bushel of Chicago wheat, feeding wheat becomes economical. Especially in quantities large enough to impact available supplies. Considering 5.750 billion bushels (bb) of corn is expected to be fed this year compared to only 120 mb of wheat, it doesn't take much of a substitution of wheat for corn in rations to have a dramatic impact on wheat supplies and ending stocks.

With July corn futures at $4.82 currently (after just challenging $5/bushel), anything less than $5.32/bushel for July Chicago wheat should attract a lot of buying interest. The latter had a low of $5.395/bushel Thursday morning, April 24. To highlight the reason for the interest from traders -- as recently as May 2024, the wheat/corn spread hit $2.53/bushel. Quite an attractive risk/reward profile.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Looking at the driving force for potential gain, old crop corn has a significant upside potential based on strong demand -- both export and ethanol production based -- amid tight supplies. For more details, see https://www.dtnpf.com/….

Technically, a double bottom on the daily chart has a target of $5.16/bushel, while a possible head and shoulders bottom formation on the weekly chart would have a target of $6.05/bushel, supported by a saucer formation. That would suggest strong buying interest around $6.55/bushel for Chicago wheat should the corn target be achieved.

As mentioned, there are many reasons to be bullish if one wants to be. The declining ending stocks estimates for major exporting countries (just like in the corn market) is a prime example. Projected to fall to a combined 36.36 million metric tons (mmt) for 2024-25 from 40.24 mmt last year, and 47.55 mmt in 2022-23, according to the recent USDA World Agricultural Supply and Demand Estimates (WASDE) update. Those countries include Argentina, Australia, Canada, the EU, Russia and Ukraine.

From a technical point of view, bottom formations developing over the last number of months are likely to inspire short covering as well given the changing risk/reward profiles.

Monthly charts show a firming off divergence bottoms where prices continue to make new lows up until July 2024 while the Relative Strength Index (RSI) did not, signaling an increase in the underlying strength.

The weekly continuation charts still have very impressive looking saucer bottom formations developing with recent lows not taking out the July lows. In general, the longer it takes a saucer to form, the more extreme the rally tends to be once prices start working higher. In this case, the current saucers started forming two years ago.

The daily chart is the most troubling, with it clearly stuck in a neutral to bear market with any attempt to rally being met by willing sellers. Given the strength in corn, that might have finally run its course based on the thesis of this post.

**

I welcome feedback along with any suggestions for future blogs. My daily comments can be found in Plains, Prairies Opening Comments and Plains, Prairies Quick Takes on DTN products.

Mitch Miller can be reached at mitchmiller.dtn@gmail.com

Follow him on social platform X @mgreymiller

(c) Copyright 2025 DTN, LLC. All rights reserved.