by

Cliff Jamieson

,

Canadian Grains Analyst

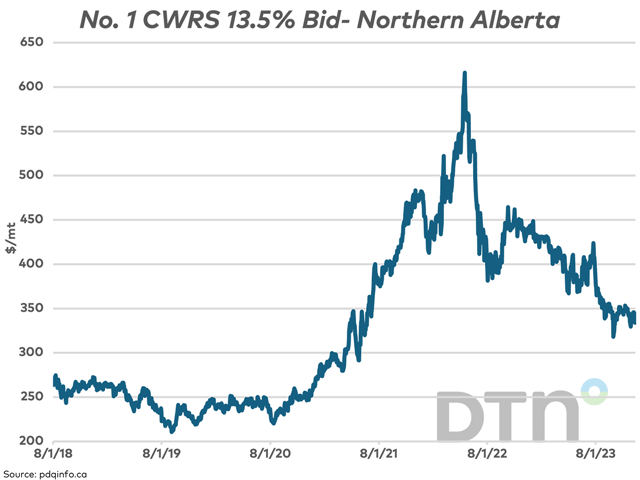

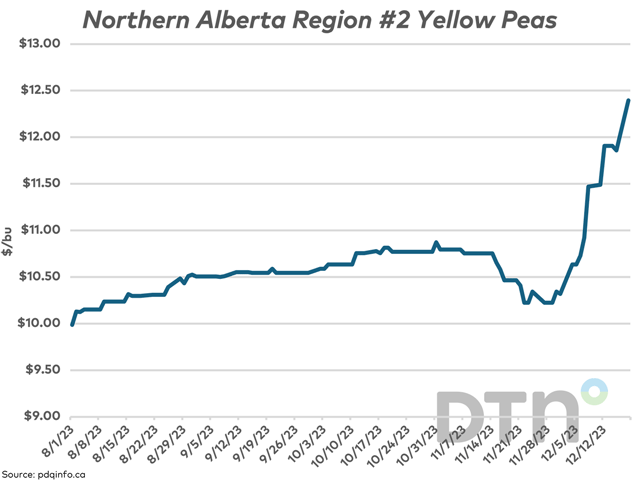

Monday's pdqinfo.ca cash bids show further upside in the yellow pea bid across most of the Prairies, while the market is inverted with a sharp drop shown for delivery in February.