Canada Markets

Ukraine Nears an End of Rapeseed Shipments

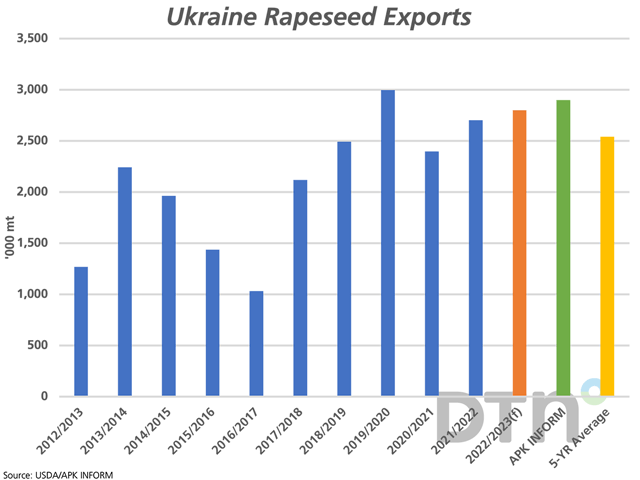

Against many odds, Ukraine's exportable supplies of rapeseed may be dwindling, with APK-INFORM reporting that 2.9 million metric tons (mmt) has been shipped during their 2022-23 crop year, which is above the USDA's estimate of 2.8 mmt of exports for the entire crop year and above Ukraine's five-year average shipments of 2.541 mmt.

Responding to high prices, Argus Media reported in mid-February that winter canola planting was up 40% from the previous year to a 13-year high and close to a record high. Despite the challenges faced in the 2022 harvest, the harvested area was reported to be 9.5% higher by UkrAgroConsult, while the USDA is estimating this area to have increased by 11% year-over-year.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

The USDA estimates 2022-23 production at 3.2 mmt, up 6.1% from the previous year and close to the record 3.465 mmt produced in 2019-20. This is despite acres lost due to the effects of the war.

The most remarkable part of this is the pace at which the crop has been shipped. Movement was off to a quick start, with UkrAgroConsult reporting in August that Ukraine's July shipments were double the pace of the previous year. Current European Union weekly data shows total imports from Ukraine totaling 2.155 mmt as of Dec. 11, up 604,737 mt or 39% from the same 24-week period in 2021-22.

Shippers and importers clearly jumped on the opportunity to move grain when it was possible to do so. Even though EU data shows total imports from all origins of 3.149 mmt as of week 24, up 37% from the same period one year ago, imports from Ukraine have maintained their share of total imports, reported at 68.4% of total imports as of week 24 which is up slightly from 67.4% reported for the same week in 2021-22.

Also linked to this news is the notion that the third-largest global exporter may soon be off of the market for the first half of 2023, with Canada and Australia remaining.

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow him on Twitter @Cliff Jamieson

(c) Copyright 2022 DTN, LLC. All rights reserved.

Comments

To comment, please Log In or Join our Community .