Fundamentally Speaking

U.S. Corn Export Shipment Pace

In past posts we have noted that corn has had quite a run since January 10 on a combination of less than expected 2013 production and far better than anticipated demand.

Price gains have been accentuated by large fund buying but this large speculative length may prove problematic should the solid fundamental underpinnings of this market start to falter.

This may have been the case last week with prices down 13 cents helped by a fall in ethanol prices.

Despite the $1.40 per gallon decline in spot ethanol futures since the beginning of April, margins are still profitable (though not insanely so as they were before). This should allow corn to hold on to some of its support.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Corn remains the cheapest ingredient to feed and with the chances of any substantial wheat feeding fading by the day, we imagine that feed demand looks on track.

That leaves exports and we have taken note of talk that despite a strong level of overseas sales that is more than double the year ago pace, shipments are lagging to such an extent that not only will the USDA not increase its export projection from 1.750 billion in subsequent WASDE reports but may actually lower it.

It is true that export shipments were lagging earlier in the marketing year based on a heavy export program for soybeans averaging 26.7 million bushels per week for the four months between the start of the marketing year September 1 to the end of 2013.

Over the ensuing four months however, they have averaged 38.5 million bushels per week and over the past month have averaged a whopping 53.7 million bushels.

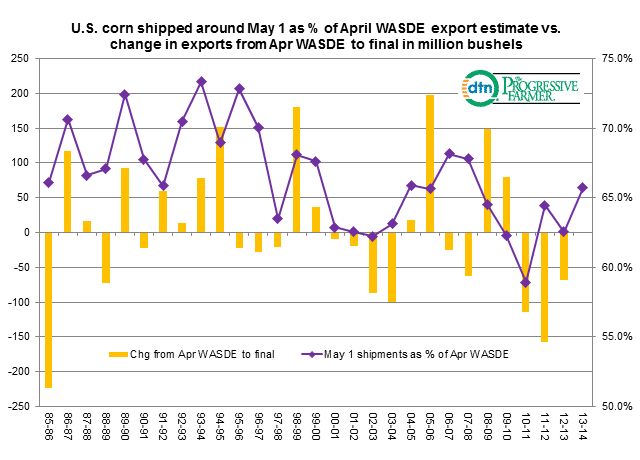

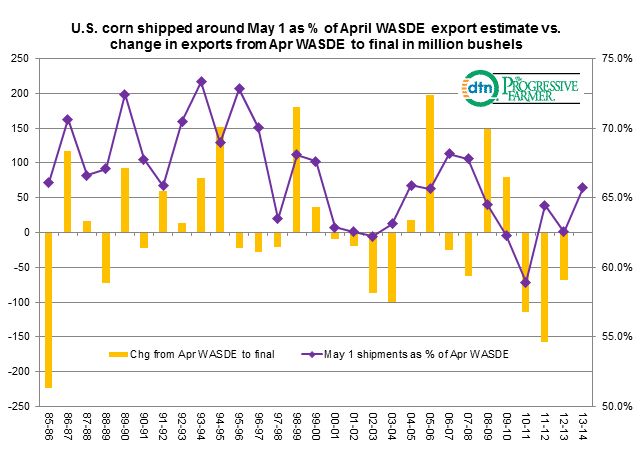

The accompanying graphic shows the amount of U.S. corn shipped around May 1 as a percent of the April WASDE export projection and also measures the change in exports from that April WASDE projection to the final figure in million bushels.

As of the first of this month, the U.S. has shipped 1.150 billion bushels or 65.7% of the April WASDE projection of 1.750 billion bushels.

This is the highest percent for this point in the marketing year since the 2007-08 season.

Is this pace fast enough to augur for a higher final figure or low enough to imply a lower foreign sales projection down the road?

Over the past three years the amount shipped as of May 1 as a % of the April WASDE has been below this year's 65.7% and each year final exports have been lower than what was indicated in the April WASDE.

The two year's prior to that in 2008/09 and 2009/10, the percent shipped as of May 1 was also lower but final exports were higher.

Given the strong sales and shipped pace seen in recent weeks, ideas that late plantings may compromise both final 2014 U.S. acreage and yields, and escalating concerns about the availability of Ukrainian corn has us convinced U.S. exports will match or even exceed this 1.750 billion figure.

Joel Karlin, Western Milling

(KA)

Comments

To comment, please Log In or Join our Community .