Fundamentally Speaking

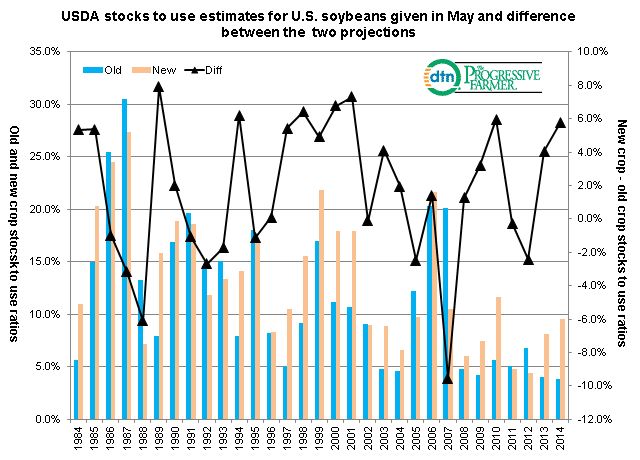

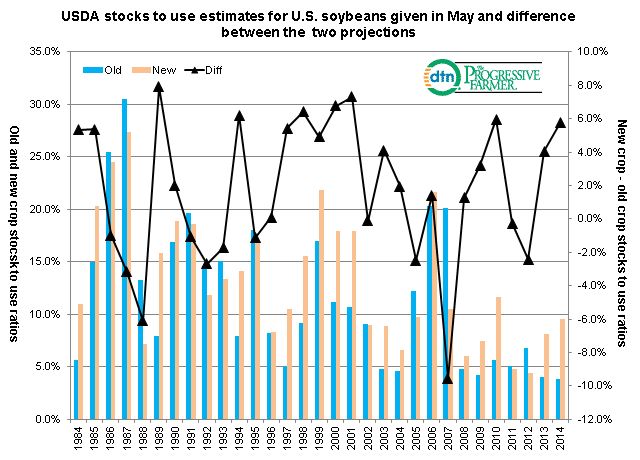

Soybean Stocks to Use Ratios

In a prior post we noted that despite the USDA issuing a very constructive old crop outlook for corn, that market had instead focused on the more bearish domestic and global new crop situation in trade action following the May 9 WASDE release.

On the other hand, the soybean complex has rallied since these numbers were released, trading more on the bullish 2013/14 situation and less responsive to the more negative 2014/15 outlook.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

This chart shows the two stocks to use ratios for U.S. soybeans in May, the first new crop forecast and what is now the 13th projection of the old crop stocks to use ratio.

The difference between the two ratios expressed by the formula new crops stocks to use -- old crop stocks to use is also provided.

This year the May old crop ratio is 3.8% and the initial new crop ratio is 9.6%, a difference of 5.7%, the largest since a 6.0% difference was seen in May 2010 and before that a 7.3% difference in May 2001.

How did the market react in those years when the first new crop stocks to use ratio implied big relief coming from a tight present day situation.

In both cases, the July-November spreads continued to strengthen even though in 2001 the November soybean contract fell starting in mid-July as the crop that year turned out well though in 2010 the November soybeans rallied all the way into expiry as that growing season was less than favorable.

Another reason why the whole price structure should remain well supported is the current stocks to use ratio of 3.8% is the lowest ever and may recede even more should current export sales on the books not get cancelled and the crushing rate stays robust.

(KA)

© Copyright 2014 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .