Fundamentally Speaking

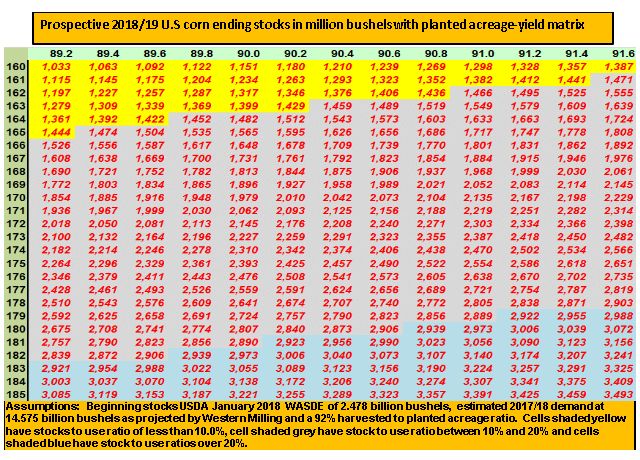

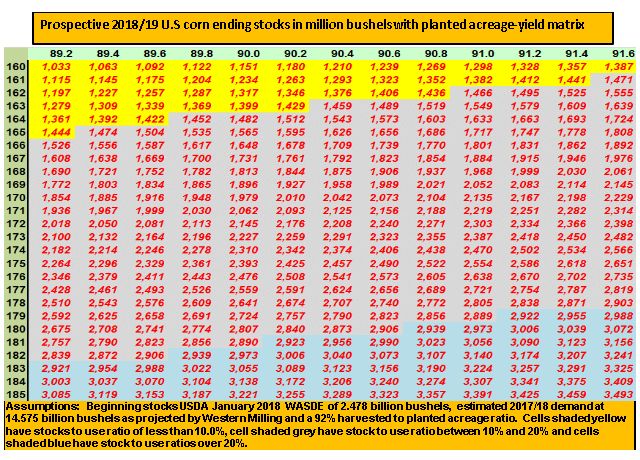

US Corn Ending Stocks/Planted Acreage-Yield Matrix

The corn market's apparent indifference to what appears to be a large drop in South American corn production this year stems from the fact that there would have to be an appreciable fall in combined Argentine and Brazilian output to have any appreciable positive impact on U.S. corn exports.

The bottom-line after the USDA's January 12th report releases include an all-time high national yield, the second highest level of production ever, record supplies, a 177 million bushel decline in total demand despite lower prices this year than last season at a ten-year low and the coup de grace of ending stocks at a 30 year high.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Given this situation, it would appear only a combination of lower yields and reduced planted area in 2018 could possibly give the corn market any support.

This matrix shows that given the largest beginning stocks since the 1987/88 marketing year along with just a modest (125 million bushels) increase in demand, just steady acreage next year, let alone any increase, combined with trend yields will result in a continuation of large stocks that will provide plenty of insurance against any adverse yields.

Such sentiments have already been detailed when the USDA released its long-term baseline assumptions late November last year.

We expect the government to confirm large supplies and relatively low prices when they release their first indication of planted and harvested acreage and yields along with their first look at the 2018/18 corn balance sheet at their annual Agricultural Forum February 22-23.

This year's stock to use ratio at 17.1% is the highest since 2005/2006 and would be maintained or even exceeded it planted corn area is close to 90 million acres and yields are able to match or exceed 176 bushels per acre.

(KA)

© Copyright 2018 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .