Fundamentally Speaking

U.S. Corn Export Projections

Ample competitor supplies and a high valued dollar are two of the reasons why our export sales pace for most grain and oilseeds is lagging the levels seen in recent years.

The USDA referenced these issues when it lowered the 2015/16 U.S. soybean export projection by 50 million bushels in last week's October WASDE report.

Eyebrows were raised however with the USDA keeping its corn export sales projection unchanged despite also witnessing a lagging sales pace.

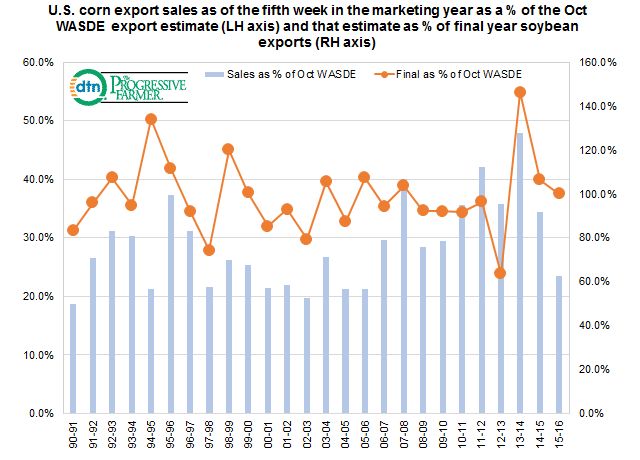

The accompanying graphic shows U.S. corn export sales as of the fifth week of the marketing year (beginning Sep 1) as a percent of the October WASDE export projection and that is plotted on the left hand axis.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

On the right hand axis is that October WASDE corn export projection as a percent of the final export figure for that marketing year.

Through the first week of this marketing year total corn export sales are 434.4 million bushels, down 28% from the year ago figure of 602.4 million bushels and the lowest total in four years.

The October 2015 WASDE report left unchanged its estimate of total 2015/16 overseas sales at 1.850 billion bushels.

This means the cumulative export sales figure is 23.5% of the October WASDE projection which is the lowest sales as a percent of the October WASDE in ten years.

Even though the marketing year is still young we were curious what a slow start to sales meant in terms of final export projections.

The evidence is mixed for the last time the early sales pace through the fifth week of the marketing year was this low was in 2005/06 at 21.3% yet final exports that season were 2.147 billion bushels, 7.4% above the October 2005 projection of 2.0 billion.

On the other hand in the 2011-12 season export sales by the fifth week of that marketing year were a relatively high 42.1% of the October 2011 export forecast of 1.60 billion yet final exports that year came in at 1.543 billion bushels or 96.4% of the October WASDE projection.

Keep in mind it is still early and with forecasted output down in some key competitors such as Argentina, Brazil and Ukraine the pace of our corn export sales could certainly accelerate in the coming months.

(KA)

© Copyright 2015 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .