Fundamentally Speaking

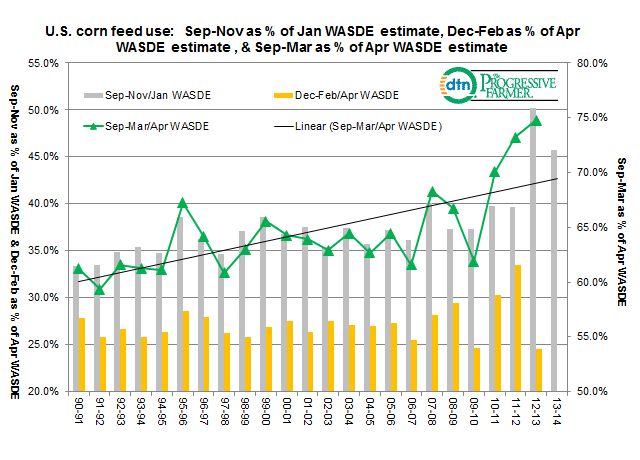

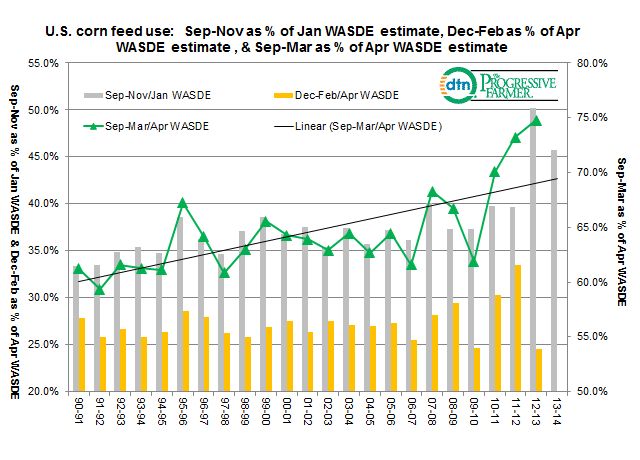

U.S. Corn Feed Use

The current rally in corn prices that has lifted futures close to 80 cents per bushel, before this week’s slight setback, started back on January 10 with the USDA posting a much lower than expected December 1st quarterly stocks figure.

Though the final 2013 U.S. corn production was 141 million bushels less than the average trade guess, the stocks number was 364 million bushels below the pre-report consensus figure implying 2013-14 feed demand 223 million bushels better.

At that time, many thought that the upcoming March 1 stocks report, to be released on the 31st would find back some of these bushels with many doubting that feed utilization is as strong as the December 1 stocks number implied.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

This graphic shows the Sep-Nov feed usage as a percent of the USDA January WASDE feed estimate, Dec-Feb feed use as a percent of the April WASDE feed projection, and finally first half feed use (Sep-Mar) as a percent of the April WASDE feed estimate.

Since the advent of the high priced corn era that we estimate to have started in 2007, the quarterly corn stocks reports have been the most volatile series that the USDA releases with the actual numbers often varying widely from trade estimates.

One big concern is that it is increasingly difficult to determine exactly how much corn is being consumed by the nation’s livestock herds and poultry flocks.

This chart shows that both first quarter (Sep-Nov) and first half (Sep-Mar) feed use has increased as a percent of the total projection over the past number of years.

This year’s Sep-Nov feed figure of 2.426 billion bushels is the highest ever and 17% above the year ago figure and represents 45.8% of the January 2014 WASDE feed estimate of 5.30 billion bushels.

This is the second highest percent ever next to the 50.2% number the year prior. First half feed use as a percent of the total year figure has increased each year for the past four and at this rate it could be 75% of the 5.30 billion figure for this season.

If that is the case, then Dec-Feb feed use should come in at 1.549 billion bushels, 43% above last year. It will be interesting to see what figure the USDA releases, but evidence suggests however that corn feed usage may be as brisk as forecast.

Even with lowest beef cattle herd since 1951 and hog numbers lowered by the PEDv disease, prices of those commodities along with milk are record high auguring for high corn feeding rates.

Brutal winter conditions in much of the main U.S. feeding areas probably resulted in higher corn inclusion rates in the feed rations for at least maintenance purposes while corn prices relative to other competing ingredients such as wheat, DDG, and corn gluten feed is very cheap.

(KA)

Comments

To comment, please Log In or Join our Community .