Fundamentally Speaking

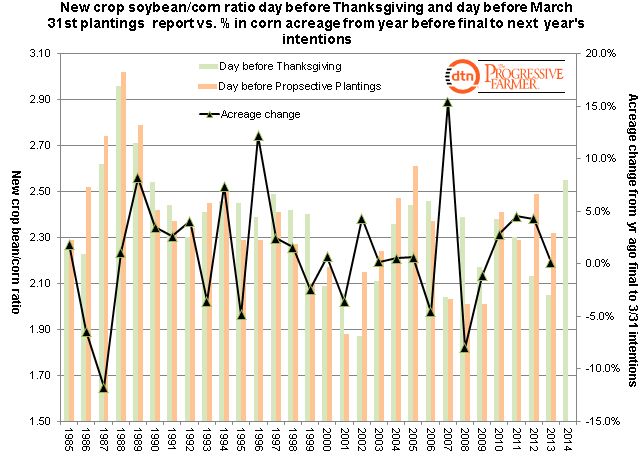

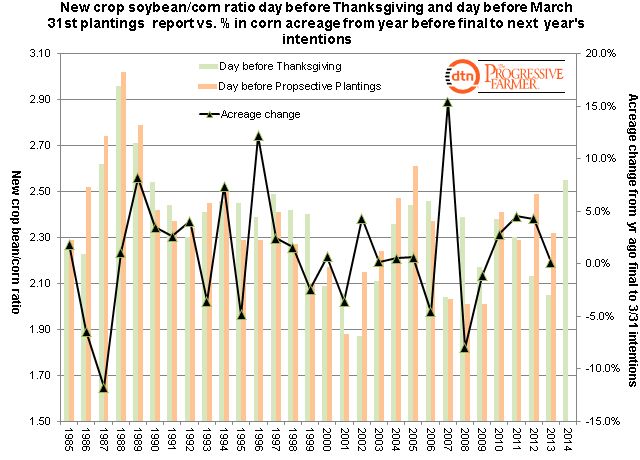

New Crop Bean/Corn Ratio History

Despite a record corn harvest that is about complete, the cash market remains very tight supported by good near-term demand and lack of farmer selling linked to a number of factors including dissatisfaction with current prices.

Producers may actually wish for current prices down the road if the situation becomes more bearish given forecasts of larger 2013 crop than currently estimated, ideas that robust demand projections may be overstated, and South American production turns out as good as advertised.

The situation becomes even more tenuous for next year as forward values may be below the estimated 2014 costs of production for some farmers.

The accompanying graphic looks at the new crop soybean-corn ratio going back over a number of years on the day before Thanksgiving and the day before the March prospective plantings reports.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

These ratios are contrasted vs. the percent change in corn acreage from the final figure of the year prior to that year’s prospective plantings report that is usually released the final business day of March.

This year the new crop soybean–corn ratio is coming in at 2.55 and that is the fourth highest figure we have in our database going back to 1985 and the highest since 1989 and well above the ten-year average of 2.27.

A general rule of thumb is a ratio at 2.35 or higher will result in a rise in soybean acreage relative to corn and vice-versa.

The current rate would imply a sharp rise in soybean acreage next year compared to corn.

There are many reasons why producers may switch some corn acreage back to soybeans including the increasing desire of farmers in the Eastern Corn belt to move back to more of a corn-bean rotation instead of going continuous corn as has been the case over the past few seasons.

There is also cognizance that corn prices may fall further as the large amount being held in storage comes to market after the first of the year.

Meanwhile despite the making of another huge South American soybean crop, uncertainty has to how well Brazil and Argentina can market that crop has kept Chinese demand for U.S. soybeans quite buoyant.

U.S. farmers may conclude that solid processor and export demand will keep soybean prices well-supported vis-à-vis corn for the foreseeable future.

This is behind talk of 2014 U.S. planted corn area at 92.0 million acres, down sharply from levels seen in 2011 and 2012 while soybean planted area next year will swell to record levels, anywhere from 80-83 million.

Keep in mind that a large drop in corn acreage next year may be forestalled by the large amount of intended corn acreage that did not get in the ground this past spring and tentative 2013 crop budgets indicating corn returns still higher than soybeans though not at the levels seen in recent seasons.

(KA)

Comments

To comment, please Log In or Join our Community .