Market Matters Blog

Typecasting Markets

In this week's On the Market column "Breaking the Rules" (available on DTN subscription sites), I talked about the four simple rules I have for analyzing markets. I also mentioned the market type table I put together for DTN more than a decade ago that I use in following the previously mentioned Rules 1 and 2. As the years have gone by, and I've mentioned the table in writing and presentations, we get asked where it appears on DTN. Well, it has no permanent home other than a dog-eared copy I have at my desk.

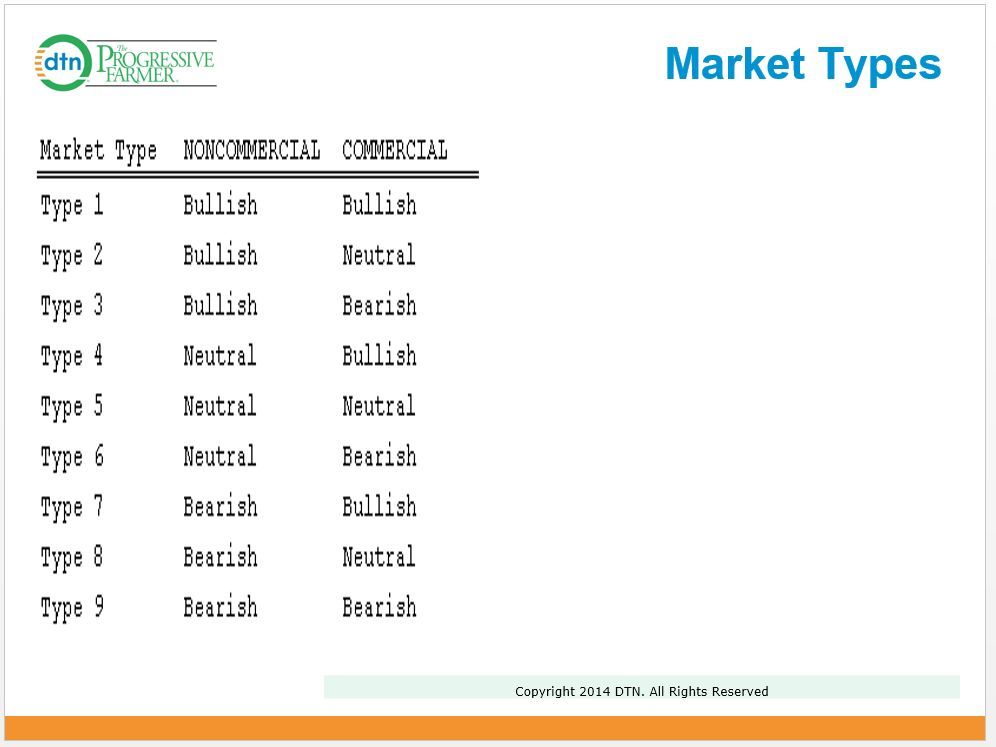

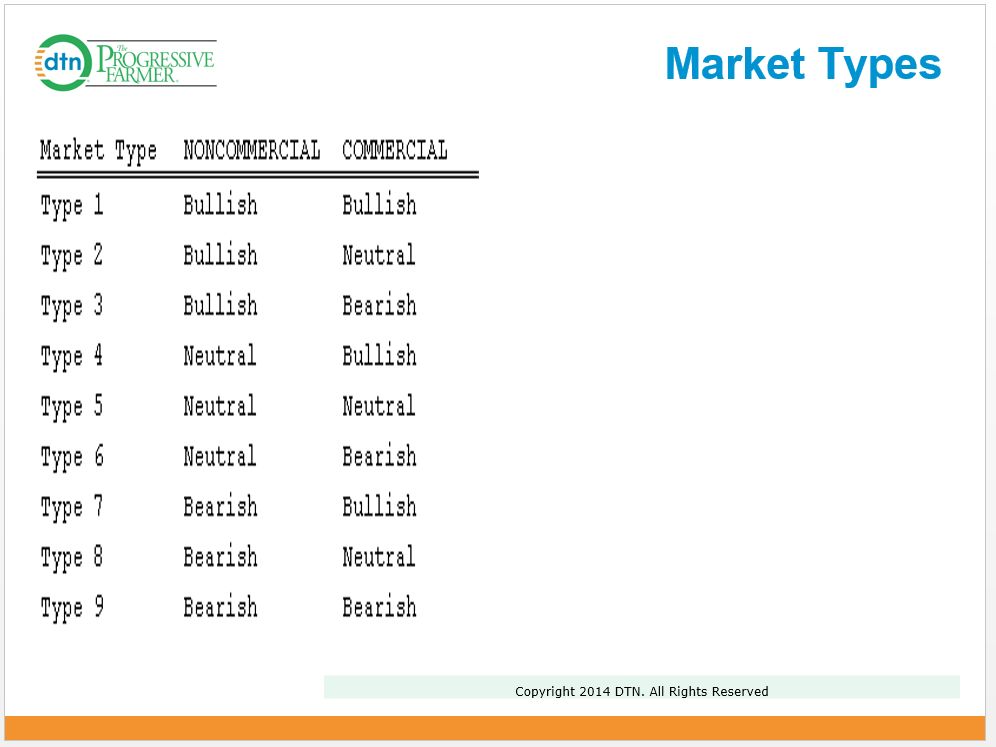

But I attached a picture of most of the table to this blog post.

Let's discuss:

I classify markets for a number of different reasons, the most important one being, because we can't always believe what we read in the news or see in USDA supply and demand tables. We need a way to block out all the unnecessary noise (yes, USDA reports are unnecessary noise) to find out what traders, both noncommercial (investment, funds, etc.) and commercial (those involved in the underlying cash commodity), really think of a particular market. We can do this by simply studying trends (price direction over time) of futures and futures spreads.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

First the trend of futures: My view differs from almost everyone else in the industry in that I believe the flow of noncommercial money into or out of a market sets the trend. Most everyone else says it is commercial activity, with noncommercials following that sets the trends. I don't see it, never have seen it, and certainly not with the evolution of computerized trade over the last 10 years or so. I watch futures trends, mostly on weekly and monthly charts, to keep track of whether or not noncommercial traders are buying or selling.

But what about fundamentals? Do I pay attention to those at all? Yes, in my own way, by tracking the trend of futures spreads (price difference between contracts of a particular market) and looking at a market's forward curve (series of futures contract prices plotted on a single line). Using mostly weekly studies, I can see how both the short-term and long-term commercial view of supply and demand is changing.

Combining these two views, noncommercial and commercial, gives us our nine different market types. Many of you might think that the two views must usually be in line with each other. But as the table shows, that only covers about one third of the market types. The rest are some variance of one or the other being bullish, neutral, or bearish, while the other is not. And it's those differences that make market analysis interesting.

Take the recent rally in crude oil for example. Investment traders came rushing to the market to buy on headlines of production cut deals within OPEC and with non-OPEC countries. This pushed the domestic West Texas Intermediate (WTI) spot futures contract to a 24% gain over the last four weeks. Meanwhile, the nearby futures spread has seen its contango (carry) increase 67 cents to $1.06 (a 58% change) over that same timeframe. Recall that a stronger contango/carry means a more bearish commercial view of supply and demand. This leaves WTI as a Type 3 market, or one where noncommercials are bullish and commercials are bearish. How do you think this sort of divergence usually ends? Do you remember the summer of 2008 when crude oil was at $140 and the media was talking $200? At the same time, the contango was strengthening, and where did WTI finish the year? That's right, down near $30.

This is just one example of how the table can be used, although there are countless others. And as discussed in Friday's column, it plays a major role in how I put together my annual market outlook I present at the DTN/The Progressive Farmer Ag Summit each December.

To track my thoughts on the markets throughout the day, follow me on Twitter:www.twitter.com\Darin Newsom

(BAS)

(AG/SK)

© Copyright 2016 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .