Canada Markets

European Countries Officially Take Canola Export Batton From China

For months now, I have pushed back against the fearmongers that suggested China would cut off Canadian imports at a moment's notice, with no reasonable alternative to take its place. That simply made no sense and Statistics Canada backed me up recently with its release of the December Canadian International Merchandise Trade data.

Very few of "the sky is falling" crowd mentioned the fact that when China basically shut out Australian barley imports in 2020 in a similar dispute, it took 18 months for the anti-dumping investigation to unfold. Nor was it acknowledged that China would want Canada's canola, given the sharp rise in palm oil values in the fall of 2024. And the idea that there would be no practical alternative made no sense, given the 29.8% (or 3.231 million metric ton) cut in global rapeseed/canola ending stocks for 2024-25 according to the USDA. I had argued that Europe would gladly take over as the primary destination following its production shortfall in 2024 -- especially with Canadian canola being on sale pricewise versus European rapeseed.

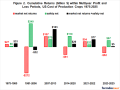

Statistics Canada confirmed those assumptions with the release of the December trade data. China had in fact slowed its imports of Canadian canola but only after importing 2.687 mmt in the first five months of the current marketing year. December imports declined to 104,890 metric tons (mt) from 427,240 mt the month before. That takes China close to the USDA's current expectation that it will reduce Canadian canola imports to 3 mmt from 5.486 mmt last year because of a lack of supply. Monthly imports averaging just 45,000 mt for the remainder of the year will let China reach that goal.

As expected, European countries took over as the primary destination with a combined 304,147 mt of canola imports for December. France alone took top spot for the month at 130,800 mt.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Given European Union production in 2024 fell 2.694 mmt or 13.5% from the previous year, the USDA expects the EU will need to increase imports by 1.393 mmt over last year (to 6.850 mmt). The problem is, "Other Countries" including Australia and Ukraine have less to export with that category's 2024-25 total exports expected to fall by 2.247 mmt. So, where will the canola come from? Canada, as much as possible, according to the USDA.

For reference regarding their capacity, in calendar year 2020, EU countries imported 2.523 mmt of Canadian canola. Clearly the greatest obstacle in the months ahead will simply be the supply of canola in Canada.

The market is certainly doing nothing to slow the process with Intercontinental Exchange (ICE) canola remaining at an unusually large discount to European rapeseed. As the production difficulties in 2024 unfolded in Europe and the Chinese anti-dumping investigation into Canadian canola was announced, the discount for canola relative to rapeseed widened to a near-record $211/mt CAD set on Dec. 17. It has since narrowed as the canola price has firmed up, but is still a $117/mt discount, above the normal range of even money to $100/mt discount for ICE canola. In short, canola is still on sale as far as Europe is concerned.

That continues to be reflected in weekly export data released by the Canadian Grain Commission. According to the weekly grain statistics report for week 27, exports have already hit 5.672 mmt compared to 3.031 mmt at the same point last year and current annual projections of 7.5 mmt. That was thanks to another strong week with 185,900 mt exported, up from 145,800 mt the week before and well over double the 73,000 mt average needed for the remaining 25 weeks. Domestic disappearance was not to be outdone with 6.194 mmt consumed in the first 27 weeks compared to 5.588 mmt last year.

Regarding the market participants themselves, the managed money traders have finally abandoned their bearish bias and have contributed to recent strength, as suggested in the recent blog https://www.dtnpf.com/…. The Commitments of Traders report released Feb. 14 by the CFTC confirmed that they had gone to a net long position for the first time since Sep. 2023, as well as marking their largest net long position since May 2022. As discussed in the blog, that sets the stage for them now to be an aggressive buyer in the canola market.

For a quick technical update -- the monthly chart still has a very interesting divergence bottom formation with the rejection of new lows in September. In that case, the price put in a new reaction low, but the Relative Strength Index (RSI) did not. On the weekly chart, bottoming formations look to be holding with the price closing over resistance at the 100-week moving average at $670/mt (May futures) as of Feb. 14. The daily chart has turned decidedly bullish with a test of resistance at $687/mt for the May contract looking very likely.

**

I welcome feedback along with any suggestions for future blogs. My daily comments can be found in Plains, Prairies Opening Comments and Plains, Prairies Quick Takes on DTN products.

Mitch Miller can be reached at mitchmiller.dtn@gmail.com

Follow him on social platform X @mgreymiller

(c) Copyright 2025 DTN, LLC. All rights reserved.

Comments

To comment, please Log In or Join our Community .