Fundamentally Speaking

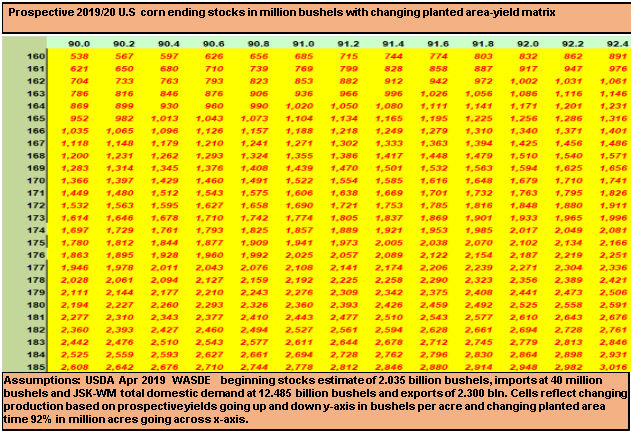

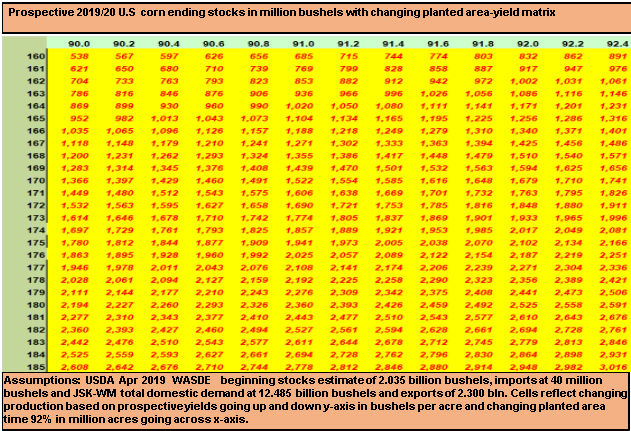

U.S. Corn Planted Area vs. Yield Ending Stocks Matrix

In a prior post, we surmised one reason for the corn market's indifference to what has been a slow start to the planting season is the realization that given an open window, farmers can seed a lot of corn in a short amount of time.

One example is the state of Illinois where seedings in 2009 and 2013 were even slower than this year's 9% as of the end of April, yet that state's final yields were quite respectable those two seasons.

Another reason is what's shaping up to be a rather bearish demand outlook both this year and next, so a loss of some intended planted acres may not have a large impact on prices.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

This chart shows prospective 2019/20 U.S. corn ending stocks matrix that has planted acreage in millions going across the x axis and yields in bushels per acre going up and down the y-axis.

Recall the USDA back in February at their Ag Outlook Forum pegged 2019/20 beginning stocks at 1.735 billion bushels (mb), but with our export pace this year slowing dramatically and the March 1 quarterly stocks implying less feed and food-seed-industrial usage (FSI), the beginning stocks number is now 300 million bushels higher at 2.035 bb.

Meanwhile, the USDA's Ag Outlook Forum estimated total demand for U.S. corn next year at 15.015 bb with total domestic use at 12.540 bb, divided between 5.50 bb for feed and 7.040 bb for food-seed-industrial usage (FSI), with next year's exports forecast at 2.475 bb.

With a record South American corn crop now being harvested and expectations that Ukraine and Russia will also harvest large corn crops for the coming year, our next year's overseas sales may be hard pressed to top this year's total of 2.30 bb, while feed demand this year at 5.30 bb could be what it is next year, so the total demand we used in the matrix is 14.785 bb.

The bottom line is that if plantings were to come in at 91.0 million acres vs. the 92.6 million acres given by the USDA in its end of March prospective plantings report and yields matched the year ago 176 bushel per acre (bpa), next year's ending stocks would still top the 2.0 bb mark.

Hence the corn market's rather tepid response to this year's slow start to seedings along with the fact that subsoil moisture levels throughout the Corn Belt are the best in years that will help carry the crop in the event that any dry spell emerges during the growing season.

(KM)

Comments

To comment, please Log In or Join our Community .