Canada Markets

Canola Basis Remains Weak

Thursday's average prairie spot delivery basis remains stubbornly weak at $34.02 per metric ton under the January, $2.35/mt stronger than reported earlier in the week, based on accessible internet bids. This is the most attractive spot basis seen since Oct. 20, but still significantly weaker than year-ago levels. It's interesting to note that both the weakest basis seen on the Prairies at $55 under and the strongest basis at $10 under are both seen at prairie crushers.

There's a list of reasons why grain has poured into the handling system, including a lack of farm storage, attractive prices, the need for drying capacity and the high volume of grain contract priced prior to harvest. As a result, year-to-date deliveries have remained high and are acting to keep demand well-fed while basis levels remain weak.

In week 16 data covering the week ending Nov. 20, 476,800 metric tons of canola were delivered into the licensed elevators over the week, a seven-week high and the fourth highest weekly volume delivered this crop year. To compare this volume to past years, this weekly volume is 56% higher than the five-year average for this week. To date, producers have delivered 6.3 million metric tons, close to 600,000 mt or 10.5% higher than the same period last year. Given the delayed harvest, cumulative deliveries had lagged year-ago volumes for the first six weeks of the crop year, while cumulative deliveries were reported to be higher than year-ago levels in eight of the next 10 weeks. The year-over-year percent increase in deliveries has increased in five consecutive weeks to week 16's 10.5%.

Commercial stocks remain high at 1.566 million metric tons, as of Nov. 20, very similar to where they were this time last year, although 33% higher than the five-year average for this time. Despite the current pace of demand being on track to achieve the current AAFC demand estimate of 18.4 mmt, both exporters and crushers are showing an overall lack of concern in obtaining supply.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

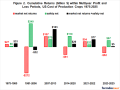

Perhaps this is best seen in basis levels in the December-through-May period, based on accessible internet bids. 2016 basis levels remain stubbornly weak in comparison to last year, as seen with the blue bars compared to the brown bars on the attached graphic. Over the six months, the widest year-to-year spread is seen in February, with the 2016 basis $11/mt wider than seen in 2015. The spread then narrows with the narrowest year-over-year spread seen in March at $7.85/mt.

It's going to take 1) a change in volumes made available by producers 2) a shock in expected 2016/17 supplies or 3) both, in order to see basis levels narrow. As indicated in a recent piece in this space, Statistics Canada has already expressed the challenges faced in tabulating this year's survey data for next week's Canadian grain production data, which means the uncertainty may last longer than wished for, which points to the continued need to watch for market signals such as basis and spreads. This also supports the rationale behind DTN's Six-Factor approach to market analysis. "The DTN Six Factor methodology is based on eliminating the noise that clouds most decision making by focusing on what the market is saying about itself," stated DTN Senior Analyst Darin Newsom.

The Thursday release of the Canadian Grain Commission's Exports of Canadian grain and wheat flour shows that farmers have also supported exports through unlicensed channels. As of the month of September, 36,863 mt of unlicensed exports have been reported, 3.6 times higher than the volume shipped in the same period in 2015.

**

DTN 360 Poll

This week's poll asks what you think we can look forward to in row-crop prices (soybeans and corn) over the balance of the crop year. We encourage you to share your thoughts on this poll, found at the lower-right side of your DTN Home Page.

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow Cliff Jamieson on Twitter @CliffJamieson

(ES)

© Copyright 2016 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .