Canada Markets

Rapeseed Futures Not Finished Making New Highs

If the bullish move in the global oilseed markets is waning, someone forgot to tell rapeseed traders in Europe. The nearby February contract ended 4.25EUR higher on Friday, to close at 425EUR, despite a higher Euro trade reaching a second consecutive contract high. As seen on the attached continuous active weekly chart, the nearby February contract is nearing a test of its April 2014 high (red dashed line) at 426.25EUR.

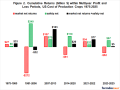

On Thursday, the International Grains Council pointed to 2016/17 world production of canola/rapeseed falling for the third consecutive year, with global consumption expected to exceed production by the widest margin in four years. Global ending stocks are estimated to fall by 20% in 2016/17, while exporter stocks are expected to fall by 14% to roughly 2.2 mmt, a four-year low. This is also supported by the USDA's estimates released earlier this month, which shows 2016/17 ending stocks of global rapeseed/canola at 5.294 million metric tons, down 1.442 mmt or 21.4% from the previous crop year while representing a tight 7.6% of annual use.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Rapeseed should be a supportive feature for canola. The continuous canola/rapeseed spread (not shown) is calculated at minus $65.29/mt USD (rapeseed trading over canola), close to the weakest spread seen over almost the past three years. Over the 2014/15 through 2015/16 crop years, this spread ranged from a high of minus $2.69/mt USD to as weak as minus $72.49/mt USD, with the average at minus $40.98/mt.

The lower-study of the chart shows a growing commercial bullishness as a supportive feature. The Feb/May spread has shown as a bullish inverse since early December (gold line), while the blue line shows old-crop gaining strength relative to new crop, as indicated in the May/August spread.

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow Cliff Jamieson on Twitter @CliffJamieson

(ES)

© Copyright 2017 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .