Canada Markets

Retail Pulse Prices Grind Lower in India

India's government has pinned large hopes on the country's recovery in agricultural output in 2016/17, after two consecutive droughts. With an overall economy expected to show a drop from 7.6% growth to 7.1% growth, agriculture is viewed as one of the bright spots which is expected to achieve a jump from 1.2% growth to 4.1% this year.

As of Jan. 13, total planting of the winter Rabi crop was estimated by India's Ministry of Agriculture at 152.3 million acres, 5.9% higher than the same date in 2016. At the same time, planting of pulses is taking place at an even faster pace, with 38.4 million acres planted, 11% higher than the same week last year, while 9.4% higher than the five-year average. Early targets set by the government show an expected 23.5% year-over-year increase in total pulses produced in the Rabi crop to 13.5 million metric tons.

An interesting editorial was found on the online site for The Indian Express titled "From Plate to Plough: Growth Amidst Gloom", which questions the Indian government's ability to sustain growth in that country's ag production. The author, Ashok Gulati, points to increases in production potentially pushing prices offered farmers to levels below the minimum support price announced by government (MSPs), while the mechanism to ensure that producers are paid the MSP is not in place. "And when government agencies fail to ensure even the MSP, the policy environment smells of an anti-farmer and pro-consumer bias," claimed the writer. The result is discouraged producers, a potential for farmers to turn away from planting certain crops and in Gulati's words "the country will remain dependent on imports of pulses and oilseeds for years to come."

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

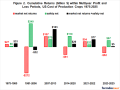

Ahead of the Rabi harvest, retail prices continue to grind lower.

The attached chart shows the trend in retail prices for just one of the many markets -- the Nation Capital Region -- or also known as the New Delhi market. This information was reported in the Weekly Bulletin on Retail Prices of Essential Commodities. Plotted is the one-year trend in retail prices for split chickpeas, whole chickpeas and split lentils, reported in India's local currency per kilogram. Chickpea prices have sunk back to levels last seen in September/October, while retail prices for lentils are reported at levels last reported in April.

In October, Bloomberg made headlines with its article "Lentil Boom Goes Bust as Crops Recoup from Canada to India"; I responded with my thoughts in "Are Lentil Prices Really a Bust?" indicating that prices had fallen from record highs although both green lentils and red lentils were significantly higher than both year-ago levels and the five-year average for that particular week.

Bloomberg has recently released a piece titled "Booming Lentil Prices are Back after Canada Harvest a Washout"; indeed, the green lentils have increased in price, with large green lentils reported today to average $66.39/cwt delivered to Saskatchewan plants, the highest price level seen since June. Current levels could one day be viewed as a gift. Trade participants have suggested there's little-or-no new export business done basis current levels, with current bids a function of position squaring needed to execute existing sales. The trend in retail prices in India is also an indicator of what's happening in that country, while a large harvest in that country could place continued pressure on this trend.

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow Cliff Jamieson on Twitter @CliffJamieson

(ES)

© Copyright 2017 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .