Canada Markets

Year-over-Year Price Change for Selected Commodities

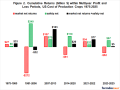

Dow Jones ran a piece today titled "In 2016, Soybeans Won, Wheat Lost, Corn Treaded Water." Here's a quick look at Dec. 30, 2016 commodity prices as compared to the last day of trade in 2015. Of the selected commodities, the winner was Malaysian palm oil, with a year-over-year increase on the continuous chart of 25.1%. Despite concerns of weakening demand, concerns of lower production in 2016 tied to the El Nino weather pattern has propelled price on the continuous chart to a recent Dec. 16 high. As seen with the brown bar on the attached graphic, price has slipped just 3.4% since reaching the December high, a continued supportive feature across the oilseeds.

The continuous chart for Paris Liffe rapeseed shows a 9.2% increase in price over the course of last year. The continuous contract reached its annual high on Dec. 15, while rapeseed futures have declined just 2.8% since and continue to act as a supportive factor in global oilseed markets.

The continuous soybean chart posted a year-over-year increase of 16.2% to the Dec. 30 close of $10.04/bu., indeed the best-performing commodity in the North American grain complex. Unlike palm and rapeseed futures, soybeans reached its 2016 high earlier in the year in June, then faced a steeper decline of 16.9% from the June high to the Dec. 30 close. DTN's top story of the year was named as the record crops of 2016 (See The Big Crops Keep Coming http://bit.ly/… ), which have weighed heavily on prices over the last half of the year.

Canola ended the year almost flat, considering a modest year-over-year increase on the continuous chart of 3.6%, from $486.50/mt to $504/mt on Dec. 30. Like soybeans, canola peaked earlier in the year (May) at $544.60/mt, while today's close was 7.5% lower than the high. Despite strong demand, the near-record crop of 2016 combined with the heavy deliveries reported in the first 20 weeks of the crop year have weighed on canola's potential.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

As a whole, wheat performed poorly, with hard red winter wheat down 10.7% over the course of the year while soft red winter wheat finished 13.2% lower (not shown). The one exception was hard red spring wheat, which ended 9.1% higher over the course of the year at $5.38/bu., although is down 4% from its $5.60 1/4 high reached in April.

Corn prices ended the year very close to where they started, having given up just 1.9% from the final price of 2015 to the final price of 2016, ending at $3.52/bu. on Friday. The year's high was reached in June at $4.39 1/4/bu., while today's close was 19.9% below the high. "Treading-water" may be the best way to view this market.

The significant growth in prairie pulse crop acres along with India's expected recovery in production following two years of drought is weighing on prices as one would expect. Bids for yellow peas delivered to Saskatchewan plants are down 36.2% from the end of December 2015 while red lentil prices are down 43.8%. Large green lentils, however, continue to show resilience and are indicated to be bid at an average price which is 2.6% higher than year-ago levels.

**

DTN 360 Poll

This week's question asks what you think is the top Canadian agriculture story of 2016? Please share your thoughts on this week's question, which is found at the lower-right on your DTN Homepage. I encourage you to drop a line to cliff.jamieson@dtn.com to share your thoughts on this subject, with feedback to be compiled for a January piece for the Canada Markets blog.

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow Cliff Jamieson on Twitter @CliffJamieson

(ES)

© Copyright 2016 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .