Canada Markets

AAFC Tweaks S&D Estimates

Agriculture and Agri Food Canada's December Canada: Outlook for Principal Field Crops report saw adjustments to 2016/17 supply and demand tables based on Statistics Canada production estimates released earlier in the month. Ending stocks for all of Canada's principal field crops were hiked close to 800,000 metric tons since November to 15.115 million metric tons. Ending stocks of all grains and oilseeds were increased close to 400,000 mt, while ending stocks of the pulses and special crops were increased by the same amount.

By far the most bearish news was seen in the estimates for durum, with 2016/17 crop year supplies increased significantly given higher estimated yields reported by Statistics Canada, while exports were pared by 300,000 mt to 4.7 mmt, up only slightly from last crop year despite the 7.8 mmt record crop produced. AAFC continues to point to higher Canadian, United States and world supplies which limits Canada's export potential, along with the lack of high quality stocks. Week 19 Canadian Grain Commission data shows cumulative exports still well-below the pace needed to reach the revised export target of 4.7 mmt, while the current carryout estimate of 2.5 mmt is up 1.4 mmt, or 127% from last year, and would be the highest volume carried out since 2009/10.

There was little change in the latest data for Canada's wheat (excluding durum). Despite a slight drop this month in expected 2016 production, both exports and ending stocks are left unchanged from last month. Estimated ending stocks for 2016/17 are pegged at 3.5 mmt, down 570,000 mt or 14% from last crop year, while just slightly lower than the volume carried out of 2007/08. As of week 19, Canada's licensed exports were roughly 920,000 mt below the steady pace needed to reach the current export target of 16.7 mmt (licensed exports only).

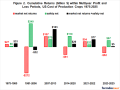

As seen on the attached graphic, stocks of both lentils and peas are expected to grow significantly over the 2016/17 crop year. Given Statistics Canada's recent yield estimates, production of peas was boosted to 4.835 mmt while exports were left unchanged from last month at 3.2 mmt. Ending stocks are expected to grow by 704,000 mt or by 400% by the end of this crop year to 880,000 mt, the highest level seen since 2009/10. One positive feature in this market is the current pace of exports, As of October's Statistics Canada Merchandise Trade data, exports were pegged at 1.5 mmt or close to 46% of the annual export target in just three months, which could see a future increase in estimated exports should this pace continue.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

While this month saw 2016 lentil production estimates fall slightly from previous estimates, AAFC reduced the export potential for the crop by 200,000 mt to 2 mmt, which resulted in a corresponding increase in ending stocks by the same amount to 600,000 mt. This is 527,000 mt or 722% higher than the tight 2015/16 carryout estimated by AAFC, which would be a three-year high. Statscan's trade merchandise data as of October shows exports at roughly 744,000 mt, well-ahead of the pace needed to reach the revised 2 mmt export target, although current projections suggest movement will slow considerably in the months to come.

This month's data points to AAFC feeling confident with their canola forecasts, with few changes made. While production was tweaked slightly higher from last month, exports, crush and ending stocks remain unchanged from November. As of last week's COPA and CGC data, both crush and exports are running at a pace which exceeds current demand projections although AAFC may be taking a cautious approach. The USDA is currently estimating Canada's canola exports to be 200,0000 mt higher than the current AAFC estimate. Canola's ending stocks are currently estimated at 2 mmt, close to unchanged from the previous crop year.

December data saw AAFC reduce seeded and harvested acres of oats from their November estimates, while boosting yields for an overall increase in 2016 production. Estimated exports were increased by 75,000 mt while domestic use was also increased, given increased supplies of lower quality which will filter into feed channels. Ending stocks were increased this month by 50,000 mt to 650,000 mt, which is 280,000 mt or 30% below the 2015/16 carryout and would leave ending stocks at a four-year low.

**

DTN 360 Poll

This week's poll asks what percentage of your 2016 production has been priced. You can respond to this poll which is found at the lower-right side of your DTN Home Page. We thank you for your input!

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow Cliff Jamieson on Twitter @CliffJamieson

(ES)

© Copyright 2016 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .