Canada Markets

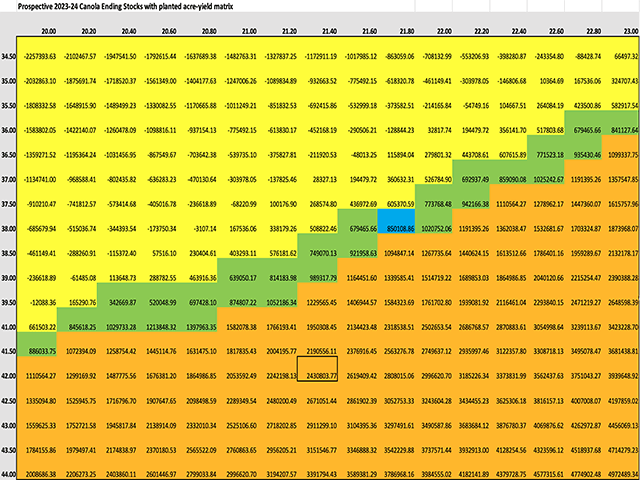

Prospective 2023-34 Canadian Canola Ending Stocks Matrix

The attached chart calculates prospective canola stocks for 2023-24, based on Agriculture and Agri-Food Canada (AAFC) assumptions in its January supply and demand estimates. The assumptions that remain fixed as acres and yield vary include 800,000 metric tons of canola carried out of 2022-23, harvested acres representing 99% of planted acres and total crop year demand of 18.550 million metric tons.

The yellow shaded area includes combinations of seeded acres and yield that result in a lower-than estimated level of ending stocks of 850,000 mt reported by AAFC in January. This is up by a modest 50,000 mt from the current crop year and is indicated by the combination of yield and acres shown by the blue shaded box.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

The brown shaded area is a combination of acres and yield where resulting stocks would be higher than the current forecast. The green shaded region represents a range where the combination of acres and yield results in the same or similar outcome as the current forecast.

It is important to note that the first forecast for the upcoming crop year is typically a cautious one. It is also interesting that the forecast increase in seeded acres is the second year-over-year increase in three years to 21.745 million acres, which follows three consecutive years of decline from 2018-19 to 2020-21. The forecast 1.6% increase year-over-year would be the smallest in seeded acres seen since the 2002-03 crop year.

The AAFC forecast yield of 2.12 metric tons/hectare or 37.8 bushels per acre (bpa) lies 0.1 bpa higher than the estimated yield for 2022 and 0.1 bpa below the five-year average for the average Canadian yield.

The current forecast for demand of 18.550 mmt represents a second consecutive year-over-year increase although is only marginally higher than the estimated demand for 2022-23. In the five years prior to the 2021-22 crop year, when demand was rationed due to a drought-reduced crop, demand averaged 20.4 mmt annually, dipping below 20 mmt only once in the five-years (2016-17 to 2020-21).

Cliff Jamieson can be reached at cliff.jamieson@dtn.com

Follow him on Twitter @Cliff Jamieson

(c) Copyright 2023 DTN, LLC. All rights reserved.

Comments

To comment, please Log In or Join our Community .