Kub's Den

Shipping Prices Back to Normal, Just in Time for Soybean Shopping

Recently, I finally got the finishing bits and pieces for a bathroom remodel that's been in the works since February. "Supply chain issues," said the contractor, a familiar refrain to anyone who's ordered anything in our post-pandemic world. My best friend mailed me a Christmas present last week, because she has been traumatized by late deliveries during the past two-and-a-half years.

Eventually, it has to get better, right? I think that time may be approaching, at least according to most of the measurable economic indicators of global shipping.

The most notorious visual symbol of the global COVID-19 shipping backlog were those container ships waiting weeks to get unloaded at the ports of Los Angeles and Long Beach -- up to 109 of them lined up at one point last January. But apparently, U.S. retailers have been planning ahead (just like my best friend) and brought in their holiday supplies already during the summer, and now the number of ships waiting for a berth in LA is down to single digits. Of course, this may be partly because some container shippers have rerouted to the Gulf of Mexico and the East Coast, specifically, to avoid the Californian congestion. Along with trucker shortages and a shaky peace between the railroads and their worker unions, it's hard to say that the supply chain problems are "over," but if it was a grain harvest we were talking about, I think we'd agree the gut slot has passed.

Many U.S. soybeans, specialty crops and value-added products get shipped to global customers in containers, so the container shipping crisis has certainly affected the agricultural shipping industry, but the more typical way commodity corn, soybeans or wheat gets to its international customers is on bulk vessels.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Crucially, the ocean freight rates for shipping bulk grain (or bulk anything) have been falling. Not always for happy, optimistic reasons, but falling, nevertheless. In USDA's latest Grain Transportation report, Surajudeen Olowolayemo identifies several influences that have hurt overall ocean freight demand: lackluster economic activity amid China's ongoing COVID-19 lockdowns, waning construction in that country, and decreased coal and iron ore imports, specifically, as well as heatwaves in Europe, typhoons in Asia and "the economic uncertainty generated by the Russia-Ukraine war."

Therefore, the price to ship grain out of the U.S., across the ocean, and into the bins of a foreign buyer has come down. It's still higher than the previous four-year average, but it's getting cheaper. Grain vessel rates from Pacific Northwest (PNW) ports to Japan, for instance, in October 2022, were seen at $36.38 per metric ton (i.e., $0.99 per bushel of soybeans or wheat). Compare that with some historical examples:

| Grain Vessel Rates, U.S. PNW to Japan | |||

| Oct-22 | $36.38 per ton | $0.99 per bushel | |

| Oct-21 | $48.13 per ton | $1.31 per bushel | |

| Oct-20 | $23.70 per ton | $0.65 per bushel | |

| Oct-19 | $28.10 per ton | $0.76 per bushel | |

| Feb-16 | $12.81 per ton | $0.35 per bushel | |

| May-10 | $41 per ton | $1.12 per bushel | |

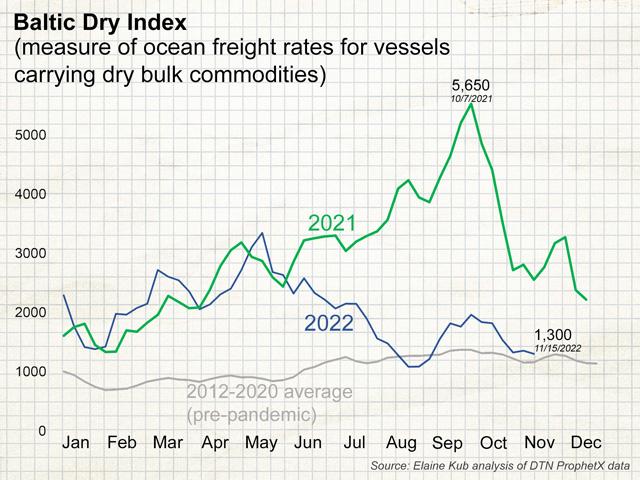

The pattern of ocean freight rates falling back toward historical norms can also be seen in the Baltic Dry Index, which is a broader index of freight prices for dry bulk goods hauled on Capemax, Panamax, Handymax and Handysize vessels. This index tracks roughly how many U.S. dollars per day are required to hire one of these vessels to haul dry bulk commodities across a various sample of shipping routes -- not just grains, but anything that can fit in the holds of these ships, and not just on a U.S.-to-Asia haul, but anywhere.

The Baltic Dry Index can serve as an indication of ship supply and financing, as was seen during a scarcity panic when the BDI reached its all-time high of 11,793 in May 2008, or during the responding oversupply and the BDI's all-time low of 290 in February 2016. Or it can serve as a measure of the globe's economic health and overall demand for dry, bulk, commodity "stuff." Since hitting a panicky post-COVID high of 5,526 last October, the index has corrected back downward and is currently at 1,300, only slightly above its pre-pandemic seasonal average for this time of year.

There's considerable uncertainty about how overall demand might continue falling for dry, bulk, commodity "stuff" amid Russian sanctions, high inflation and high energy costs. For now, however, U.S. grain shippers and the U.S. grain markets will find the newly re-normalized ocean freight environment supportive to domestic grain prices.

Cheaper international freight can counteract the effects of a strong dollar to keep U.S. grain affordable for end users (or at least relatively less unaffordable). Consider that, if cash corn at the PNW is $8.69 per bushel, adding $1.31 of ocean freight would put the price tag to a Japanese buyer at $10 per bushel. If the freight cost is only $0.99, as it is now, at least the price tag stays in the triple digits. However, as ocean freight gets cheaper, it also becomes easier for grain shippers to switch commitments from one origin to another (i.e., taking South American grain from South American ports instead of taking U.S. grain from U.S. ports).

Therefore, it seems, for now, we can plan our Black Friday and Cyber Monday shopping sprees with confidence, but the supply chain and freight cost scenario bears watching as global demand becomes clear.

**

Comments above are for educational purposes only and are not meant as specific trade recommendations. The buying and selling of grain or grain futures or options involve substantial risk and are not suitable for everyone.

Elaine Kub, CFA is the author of "Mastering the Grain Markets: How Profits Are Really Made" and can be reached at masteringthegrainmarkets@gmail.com or on Twitter @elainekub.

(c) Copyright 2022 DTN, LLC. All rights reserved.