Kub's Den

A USDA Report About a Report About Reports

The weekly Broiler Hatchery report, the monthly Cattle on Feed report, the North American Grain and Oilseeds Crushings report, the Peanut Prices report ... USDA's National Agricultural Statistics Service (NASS) sure keeps busy releasing reports! But there was one largely ignored annual report buried in the onslaught this month, which deserves a closer look: the annual "Price Reactions After USDA Crop Reports" report.

NASS releases a similar report about price reactions after USDA livestock reports, but let's just focus on one thing at a time. Does it look like grain prices are predictably swayed by government numbers?

USDA collects evidence about this question to show that they're not exerting undue influence on prices with their statistics releases. Ultimately answerable to the American people, presumably the department doesn't want to undertake actions that are exploitable by traders at the expense of agricultural producers or grocery shoppers. If the report shows no historical evidence of predictable price movement, then we can reassure ourselves the markets aren't being set up for some kind of manipulation next Wednesday, March 31, when we'll get a big dump of grain market-related statistics: Agricultural Prices, quarterly Grain Stocks and the results of the annual Prospective Plantings survey.

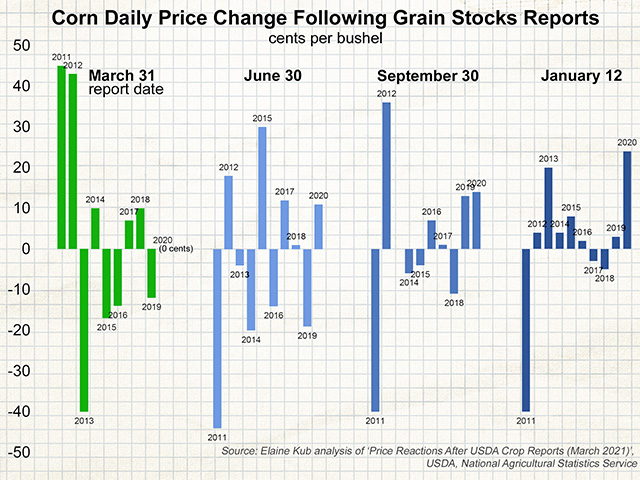

The "Price Reactions After USDA Crop Reports" report looks at the cash grain prices of corn, soybeans, wheat and cotton on the day before certain reports, then compares them to the prices at the end of the day once each report is released, as well as the prices one week after each report. The only reports it studies, however, are the Crop Production reports (released for row crops in August, September, October, November and an annual summary in January) and the quarterly Grain Stocks reports (March 1 data released at the end of March, June 1 data released at the end of June, Sept. 1 data released at the end of September and Dec. 1 data released in the middle of January). The report therefore doesn't study price reactions to the monthly World Agricultural Supply and Demand Estimates (WASDE) reports, which are more ephemeral economic projections from a different branch of USDA, instead of these dollops of hard, surveyed data from NASS.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Anyway, the takeaway is there is no real pattern in the price reactions. These USDA reports are not consistently driving grain prices up or down. Following each quarterly Grain Stocks report since 1985, the market has displayed 69 daily price increases, compared to 71 daily price losses and eight "no change" days. Similarly, impartial distributions of up-and-down reactions have been noted for soybeans, wheat and cotton after both Grain Stocks reports and Crop Production reports, looking at day-after and week-after price reactions. If anything, the count across all crops, all reports and all timeframes may show a tiny bias toward downward price reactions (1,141 increases, 74 no changes, and 1,155 decreases), but not to a statistically significant degree.

Focusing just on corn and just after the quarterly Grain Stocks reports in the past 10 years, it does seem like March is the timeframe to expect big reactions, one way or another. After the March 30, 2012, report date, for instance, corn prices rose 43 cents (7%) in one day and 61 cents (10%) in one week. The next year, after the March 28, 2013, report date, corn prices lost 40 cents (5%) in one day and 96 cents (13%) in one week. Overall, the absolute value of the March report's one-day price movement tends to be about 4% either up or down; after the first week of April, corn prices have averaged a 5% change one way or another.

June quarterly Grain Stocks reports trigger similar-sized price movements in corn, but the September and January Grain Stocks reports tend to bring about smaller price changes -- only 2% to 3%, one way or another, either after a day or after a week.

Cleverly, USDA's report about reports doesn't just measure futures price movement. No, the "corn price" they use is "the closing cash price for Southern Iowa #2 yellow corn," which means their study is able to detect report influences on basis movement (in a sample of one region's bids), as well as the underlying futures price movement. Consider the March 31, 2011, movement, when after bullish reports the nearby May futures contract ended the day locked limit up, 30 cents higher, at $6.93 1/4. USDA's data shows the cash corn price rose 45 cents that day -- or 15 cents of basis strengthening alone. Just a reminder for next week: the daily price limit is $0.25 per bushel for CME corn futures these days and $0.70 per bushel for soybeans.

If the March 31 trading date has a history of relatively bigger moves than other months, that's hardly surprising because March 31 is not only the date of the quarterly Grain Stocks report release, but also the release of the annual Prospective Plantings survey results. Both are servings of fresh information to a market that has no other official way to obtain nationwide grain inventory levels or comprehensive farmer planting intentions. The two reports address two separate crop years: the inventory of how much of last year's grain is still sitting in bins and the potential number of acres that might grow various types of grain once planted this spring. But the bullishness or bearishness of each report can definitely influence the trading patterns of both nearby and deferred futures contracts. Unfortunately, it's impossible to isolate the effects of either report separate from each other. We can't "control" the experiment and see if the market would jump 5 cents for the Prospective Plantings report but drop 15 cents once the influence of the Grain Stocks report was also factored in. There's just no way to know, because both will be released at the same moment: 11 a.m. CDT on Wednesday, March 31, 2021.

There was one reliable pattern I could see in the data. We may not be able to predict from history whether grain prices are more likely to go up or down on Wednesday, March 31, but history does suggest if corn prices close up that day, by the Wednesday of the following week they will likely still be higher than their Tuesday, March 30, price tag. It's been very rare in the past 10 years that the market doesn't remain either "up" or "down" for a week after a quarterly Grain Stocks report, especially if the report's one-day reaction was a double-digit jump. In fact, after March reports specifically, this has been true every year for the past 10 years -- but let me emphasize this is just an interesting little bit of trivia, not a trading recommendation.

And perhaps it's not a good idea to get too eager about the idea of big March 31 market movements. In the cash corn market, the price change on March 31, 2020, was exactly 0 cents.

Elaine Kub is the author of "Mastering the Grain Markets: How Profits Are Really Made" and can be reached at masteringthegrainmarkets@gmail.com or on Twitter @elainekub.

(c) Copyright 2021 DTN, LLC. All rights reserved.