DTN Fertilizer Outlook

Wholesale Fertilizer Prices Higher in July

July proved to be a surprisingly strong month for fertilizer prices in the U.S., during a time which is typically slower with post-spring season refill buying and the beginning of the off-season in agriculture markets while the spring crop grows. Phosphates and urea saw notable strength last month. Specifically, DAP and MAP markets saw prices increase and the unusual DAP-to-MAP premium reverse after prices began to buck the historical trend late last year.

The following is a recap of fertilizer price trends and market developments for July:

AMMONIA

Domestic: Fourth-quarter ammonia prepay offers were announced by producers in mid-July this year at initial levels ranging from $385-415 per short ton (t) ex-works (price a buyer of a shipped product pays for the goods when they are delivered to a specified location) in the Corn Belt and $360-410/t ex-works at Oklahoma-area production facilities.

In comparison, prepay offers in Iowa were announced last year at the end of July at $900/t ex-works Port Neal for Q4. Oklahoma plant offers were also significantly higher in 2022 at a range of $850-875/t ex-works. Nebraska volumes were posted similarly higher at $925/t ex-works.

Following the prepay deals offered, there was little other news in the U.S. ammonia market following the higher settlement at Tampa for August announced before the end of July.

Prompt offers at the end of last month were still understood to be offered around $390/t free-on-board Illinois (FOB -- or sales price with any additional transport costs paid by the buyer), lower from Q4 sales earlier in July which were offered from $385-435/t in the Corn Belt.

Meanwhile, Eastern Oklahoma-area ammonia producers were also heard offering at levels around $300/t ex-works, unchanged following the Tampa price for August edging up by $10.

International: At the end of July, Yara and Mosaic settled at $295 per metric ton (mt) cost-and-freight (CFR -- sales price with freight costs to buyer included) Tampa for August deliveries. This was up $10/mt on the $285/mt CFR the parties previously agreed for July deliveries at Tampa.

The higher assessment at Tampa falls in line with market sentiment that ammonia prices have for the moment reached their lowest point of 2023.

However, offsetting this expectation slightly is demand from northwest Europe is limited, and with gas prices in the region relatively low, there is an expectation that major ammonia producers in Europe will increasingly opt to make rather than buy. Prices in the region consolidated within the end-June price range of $330-360/mt CFR duty-paid to July's last assessment of $350-360/mt CFR.

Ammonia prices in the Black Sea continue to be assessed nominally on account of little export activity from the region given the ongoing armed conflict, assessed flat at the end of last month from June prices of $270-275/mt FOB.

The price outlook in the global ammonia market coming out of July was stable to firm across the globe.

UREA

Domestic: U.S. urea barge trading in New Orleans (NOLA) at the end of July reached $360-410/t FOB, up from trades in the preceding month in a range of $285-317/t FOB. Shorter availability of both available urea volumes, as well as dry bulk river barges in the U.S. Gulf, have continued to support higher fertilizer values despite slowing nitrogen demand compared to the peak of spring activity.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

River terminal equivalent values at the higher NOLA levels ranged from roughly $440-475/t FOB, higher compared to end-of-June offers at $420-475/t FOB at the same primary river terminals including St. Louis, Tulsa and Cincinnati.

Following a more bearish sentiment in the global market emerging as India's urea demand is increasingly fed by China, U.S. urea prices were expected to remain under pressure in the U.S. Gulf. However, the need for more resupply volumes following spring activity clearing out inventories could continue to provide some upside to price levels.

International: The global urea market was mixed last month on account of production cuts in Egypt being somewhat balanced by the question of how much urea export capability China possesses at the moment in view of India returning to market with a fresh purchase tender.

Egyptian sales levels increased following the news in the market that natural gas cuts were being enforced throughout the country, reducing available inputs to produce urea. At the end of July, we assessed the country's granular export market in a range of $422-440/mt FOB, up sharply from the prior month's assessment of $340-350/mt FOB.

In Brazil, some demand emerged and the increased buying raised our assessment to $410-420/mt CFR last month -- a steep increase from end-June price levels of only $290-315/mt CFR.

At the end of July, the market continued to rally with Egyptian production cuts and a fresh Indian tender, offset only by uncertainty around China's ability to export significant quantities. Brazilian demand also provided the market with some structural support.

UREA AMMONIUM NITRATE (UAN):

NOLA UAN barge prices firmed to $220-225/t FOB last month, up from our last assessment for June of $180-220/t FOB following higher offers from sellers after summer fill offers were pulled last month.

Offers on UAN 32% were released in the first half of July at $195/t FOB NOLA, basis Cincinnati netback, and equivalent offer levels at U.S. river terminals. Eastern Oklahoma area nitrogen plants offered between $205-210/t ex-works as part of the sales programs, down from offers at $240/t ex-works prior to the announcements. CF at its Port Neal, Iowa nitrogen facility offered $220/t ex-works in the first round of announcements before offers rose to $230/t.

On the follow to the fill programs, offers were raised $25-30/t over initial announcement prices. River terminal offers on UAN 32%, for example, moved higher to $255-260/t FOB for prompt tons at hub markets including St. Louis to Cincinnati, up from the summer fill offer level at $225/t FOB for Q3 tons while prices were valid.

With a strong pace of exports from the U.S. expected for the remainder of the year, inbound supplies are expected to be similarly reduced with more competitive prices for UAN in South and Latin America as well as Europe. UAN prices are thus positioned to see more support in the second half of 2023. Although, if fall weather allows for a large-scale application of anhydrous ammonia this year, UAN demand for the spring could be impacted.

PHOSPHATES

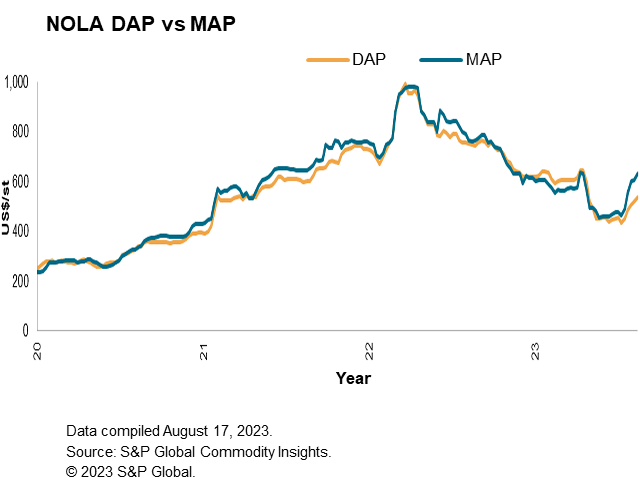

Domestic: Phosphate prices in the U.S. began to run up at an incredible rate in July after falling lower to begin the month. Short supplies after summer meant buyers paid higher prices for what few volumes were available, and the fall shipment lineup to the U.S. from exporters such as Saudi Arabia, Australia and Jordan began to increase. The inverse-premium of DAP against MAP seen earlier this year also saw a sharp correction to more typical spreads as a result.

NOLA DAP for instance was assessed $470-500/t FOB at the end of July, up from the previous weekly assessment of $445-460/t FOB, but lower from our end-July assessment of $515-646.

MAP prices were adjusted higher over DAP to a range of $525-560/t FOB, and higher from $474-480/t at the end of June.

River terminal phosphate prices ended July offered from $520-530/t FOB MAP and $490-495/t DAP across main terminal hubs on a lack of much buying interest compared to U.S. Gulf barges. June terminal offers in comparison were $520-550/t FOB MAP and $495-530/t FOB DAP.

The outlook on domestic phosphates prices was poised to remain stronger heading into the fall with more imports needed to replenish stocks drained during the spring season.

International: With little product uncommitted for shipment during the coming weeks, DAP and MAP prices are firm from all origins and the level of activity in DAP and MAP markets was limited at the end of last month. Where there has been action, prices have risen as shown in the U.S.

In fact, at U.S. price levels at the end of July, Moroccan exporters were theoretically fetching better returns by shipping cargoes to the U.S. instead of Brazil, even taking the current duty rate of around 15% into account.

Elsewhere, in the world's largest import market for phosphates, Indian DAP fell marginally to $445-448/mt CFR compared to a flat price of $455 CFR in the previous month. Purchases have been somewhat deferred with the current subsidy program ending next month, but buyers seem willing to engage at these levels.

The real strength in the market was seen in the Americas, like in Brazil where MAP prices reached $485-490/mt CFR at the end of July, up from June's weaker market which saw prices ranging from $430-440/mt CFR.

Pricing appears set to remain firmer in the short term across all geographies.

POTASH

July saw the much-anticipated summer fill programs announced from North America's largest producers, as well as surprises in the form of Canadian port worker strikes which had potentially much more significant implications for the international market.

Last month, barge prices ended July assessed from $310-334/t FOB, lower compared to the prior month's assessment of $390/t FOB with potash summer fill programs being announced.

The sales programs were said to receive strong uptake from buyers after releasing at a low $300s/t FOB NOLA equivalent. Mosaic saw a strong pull on its North American potash fill program upcountry at posted prices and was offering NOLA barges at $335/t FOB NOLA toward the back half of its sales program.

Prices came out toward the lower end of market expectations heard in discussions at last month's annual Southwestern Fertilizer conference in Denver, and the long-awaited announcement seemed to receive robust participation across the country.

River terminal offers for granular MOP ahead of the fill were posted from $380-410/t FOB compared to $395-430/t FOB earlier in July. Following the programs, volumes were offered as low as $350-360/t FOB with deeper discounts reported in southern U.S. markets.

It seems that the Canada port strikes did not have as much of an impact on the global market as feared with the situation resolved for now. Prices are expected to remain somewhat stable in the short term as potash producers, including Nutrien, roll back planned production increases in response to a weaker-than-expected price environment.

**

Editor's Note: This information was supplied courtesy of Fertecon, S&P Global Commodity Insights.

(c) Copyright 2023 DTN, LLC. All rights reserved.