USDA Reports Preview

May WASDE Offers First Guess of 2026 Crops

At 11 a.m. CDT on Tuesday, May 12, USDA will release the May edition of Crop Production and the World Agricultural Supply and Demand Estimates (WASDE) reports. It is a unique report because it features the first look at 2026-27 balance sheets for corn, soybeans and wheat.

CORN

The corn market enjoyed a strong finish to the month of April, reaching 2026 calendar year highs for new-crop December futures while old-crop July prices tied their highest mark thus far on May 5. Through the past week, however, prices have been pressured by technical-based selling along with risk-off trade stemming from reports of progress potentially being made in restarting negotiations between the U.S. and Iran, though that remains to be seen. For Tuesday, traders will shift focus back to fundamentals, where the corn market is very likely to reflect healthy worldwide supplies.

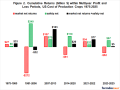

Beginning on the old-crop side of the equation, USDA will take another look at demand categories. As a bullish note, the record pace for corn exports is undeniable, with commitments as of April 30 surpassing the 3-billion-bushel (bb) mark and 29% ahead of the same point in 2025. USDA is expecting a 15% year-over-year increase in corn exports to 3.3 bb. Meanwhile, through March, the amount of corn used for ethanol is running less than 1% ahead of the same point in 2024-25, with USDA expecting a 3% increase. As mentioned in previous writings, I also remain skeptical of the record-large feed and residual USDA is currently penciling for 2025-26. All totaled, I have an upward bias toward 2025-26 U.S. corn ending stocks, and the 14 analysts surveyed by Dow Jones appear to agree, with an average guess of 2.140 bb compared to 2.127 bb in the April WASDE.

Jumping to new-crop 2026, it is very likely that USDA will use the 95.3 million acres (ma) of corn found in the March Prospective Plantings survey, combined with a trendline yield of 183 bushels per acre (bpa). Assuming the same harvest ratio in the February Ag Outlook, would give a 2026 corn production estimate of 15.974 bb. This would be down roughly 6% from last year's record crop. On the demand side, it is difficult to gauge this far in advance, but history would suggest lower supply means slightly lower demand (typically as a result of a higher average price). The Dow Jones survey expects 1.960 bb of U.S. ending stocks by August 2027, which would imply roughly 16.2 bb of demand compared to 16.47 bb this year, which seems reasonable.

Within the world market, the focus will once again be on South America. The wet season in Brazil ended a couple of weeks early this year, leaving a good portion of the safrinha corn crop hot and dry through pollination. While the jury is still out on that, it's important to remember that USDA's 132 million metric ton (mmt) estimate from April is quite a bit lower than many others, including CONAB at 139.6 mmt. For this reason, traders see the USDA forecast rising to 133.7 mmt in Tuesday's report. Meanwhile, in Argentina, USDA is now well below local estimates, which range from 61 mmt up to 67 mmt. The Dow Jones survey has the crop at 56.2 mmt and up from 52 mmt in the April report. As a result, world corn ending stocks are expected to rise moderately to 296.5 mmt. For the new 2026-27 season, ending stocks are expected to fall to 286.7 mmt, largely driven by the changes in the U.S., and it is of course still very early to draw overly confident conclusions on world supplies for the next year.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

SOYBEANS

Since the last WASDE in early April, soybean futures have traded in a mostly sideways pattern, with July futures roughly 7 cents higher than the April 9 close at the time of writing this. Meanwhile, new-crop futures have enjoyed a bullish month, hitting new calendar year highs in early May for the November contract. While President Trump's visit to China on May 14-15 is arguably the most pivotal upcoming event for the soybean market, traders will tune in on Tuesday for USDA's take on supply and demand.

For the 2025-26 season, demand continues to be a mixed bag. On one hand, crush premiums are near record levels thanks to three-and-a-half-year highs in soybean oil futures. Through March, the volume of soybeans crushed through the marketing year was 8.6% ahead of the same point in 2024-25, with USDA currently forecasting a 6.7% year-over-year increase to 2.610 bb. On the export side of things, commitments as of April 30 are 1.430 bb, down 18% and even with USDA's full-year expected decline. With four months remaining in the marketing year, achieving 110 million bushels (mb) of sales and 220 mb of shipments to hit USDA's goal by no means appears unattainable, but will need to be monitored closely. For Tuesday, I expect minimal changes to the old-crop outlook, and stocks could very well remain near 350 mb. The analysts surveyed by Dow Jones are expecting 347 mb on average. For the new-crop outlook, using the March Prospective Plantings area estimate of 84.7 ma and a trendline yield of 53 bpa would result in a 4.436 bb crop, up 4% from 2025, if true. On the demand side, I expect USDA to forecast a recovery from the 13-year low in export demand set in 2025-26, while crush will very likely expand to another record. The Dow Jones survey estimate for 2026-27 ending stocks of 353 mb would imply demand near 4.453 bb, also 4% improved from 2025-26.

For the world update, the old-crop season should feature only fine-tunings to USDA's estimates for world crops. That being said, traders are expecting a slightly higher Brazilian crop to 180.4 mmt, and an upward revision to Argentina's production as well to 48.5 mmt. As a result, stockpiles are expected to grow to 125.6 mmt and reclaim their place as the largest world soybean reserves on record. However, traders are not expecting that record to be held for long, anticipating 126.3 mmt of reserves for the upcoming 2026-27 season. For what it's worth, in their March Oilseed annual reports, the USDA attache in Brazil forecasted another year of growth in planted soybean area and a crop of 184 mmt. For Argentina, USDA is expecting acreage to increase by 5% in 2026-27, but were conservative on yield, resulting in only a slight increase in production to 49 mmt.

WHEAT

On April 9, the day of the last WASDE report, July Kansas City wheat futures closed at $6.05 3/4. Since then, declining winter wheat conditions in the U.S. and ongoing fertilizer constraints out of the Persian Gulf sent futures skyrocketing to a high of $7.18 1/2 on April 29. Since then, futures have turned lower on a combination of technically inspired profit-taking and reports of renewed peace proposals in the Middle East. On Tuesday, traders will get a much-anticipated look into where USDA sees U.S. wheat production landing in 2026 amid widespread drought.

To start with the old-crop 2025-26 season, which is set to end on May 31, I don't expect drastic changes from the April report. As a positive note, wheat export commitments as of April 30 are 910 mb, ahead of USDA's goal of 900 mb. However, shipments will need a strong finish to reach the goal, otherwise some sales will likely carry over into the new season. Analysts surveyed by Dow Jones combined for an average guess for 933 mb of wheat stocks as of June 1, which I would agree with as a fair assumption. For new-crop production, the average trade guess is calling for 1.731 bb between winter and spring wheat varieties, with none of the varieties expected to outperform 2025's crop amid historically low area. Personally, I'm using a 1.735 bb crop, which is right in line. The Dow Jones survey results for ending stocks of 841 mb would imply a slight decline in total wheat usage, although the silver lining there is that would likely need to be the result of a higher price as compared to the five-year lows seen in 2025.

For world wheat, no major changes are expected for the old 2025-26 season, with world reserves expected to be similar to April's update at 283 mmt. Moving ahead to 2026-27, and analysts are expecting a minor decline in stocks to 281.2 mmt. In their April Grain and Feed annual reports, USDA already forecasted anticipated production declines from a record-setting 2025. With Argentina, Australia and Canada expected to fall annually by 25%, 19% and 10%, respectively. As is usually the case with the world wheat balance sheet, it will be important to monitor overall production and trade trends rather than stocks themselves, which can be misleading given the large reserves held by countries such as India and China, which are typically closed off to world trade.

**

Join us for DTN's post-report webinar at 12:30 p.m. CDT on Tuesday, May 12, as we discuss USDA's new estimates in light of recent market events. Questions are welcome, and registrants will receive a replay link for viewing at their convenience. Register here for Tuesday's USDA WASDE webinar: https://www.dtn.com/….

| U.S. PRODUCTION (Million Bushels) 2026-27 | |||||

| May | Avg | High | Low | ||

| Corn | 15,948 | 16,011 | 15,819 | ||

| Soybeans | 4,450 | 4,521 | 4,405 | ||

| All Wheat | 1,731 | 1,833 | 1,653 | ||

| Winter | 1,201 | 1,375 | 1,130 | ||

| U.S. ENDING STOCKS (Million Bushels) 2025-26 | |||||

| May | Avg | High | Low | Apr | |

| Corn | 2,140 | 2,267 | 2,077 | 2,127 | |

| Soybeans | 347 | 370 | 320 | 350 | |

| Wheat | 933 | 962 | 912 | 938 | |

| U.S. ENDING STOCKS (Million Bushels) 2026-27 | |||||

| May | Avg | High | Low | ||

| Corn | 1,960 | 2,110 | 1,776 | ||

| Soybeans | 353 | 475 | 300 | ||

| Wheat | 841 | 955 | 760 | ||

| WORLD ENDING STOCKS (million metric tons) 2025-26 | |||||

| May | Avg | High | Low | Apr | |

| Corn | 296.5 | 300.4 | 293.0 | 294.8 | |

| Soybeans | 125.6 | 127.0 | 123.7 | 124.8 | |

| Wheat | 283.0 | 284.0 | 282.0 | 283.1 | |

| WORLD ENDING STOCKS (million metric tons) 2026-27 | |||||

| May | Avg | High | Low | ||

| Corn | 286.7 | 301.0 | 268.0 | ||

| Soybeans | 126.3 | 132.6 | 122.1 | ||

| Wheat | 281.2 | 291.0 | 275.0 | ||

| WORLD PRODUCTION (million metric tons) 2025-26 | |||||

| May | Avg | High | Low | Apr | |

| CORN | |||||

| Argentina | 56.2 | 60.0 | 52.0 | 52.0 | |

| Brazil | 133.7 | 137.0 | 130.0 | 132.0 | |

| SOYBEANS | |||||

| Argentina | 48.5 | 49.0 | 48.0 | 48.0 | |

| Brazil | 180.4 | 181.6 | 180.0 | 180.0 | |

Rhett Montgomery can be reached at rhett.montgomery@dtn.com

Follow him on social platform X @R_D_Montgomery

(c) Copyright 2026 DTN, LLC. All rights reserved.