DTN Fertilizer Outlook

Wholesale Ammonia Prices Forecast to Rise on Tight Supplies, Expected Good Fall Application Period

The following is a recap of fertilizer price trends and market developments for the month of September.

AMMONIA

Domestic: September was a month of firming prices in the U.S. ammonia market. Increases were attributed to a near-record year of sales for prepaid ammonia, according to market participants for the fall, as well as several nitrogen plants going down, including OCI's Weaver, Iowa, site and others in the U.S. Gulf.

Following a sharp increase in the Tampa ammonia contract between Yara and Mosaic, Corn Belt prices in the U.S. increased at the end of September to around $700-$725 per short ton (t) free on board (FOB -- sales price per ton without transportation costs included), up from $625-$650 earlier in the month.

Eastern Oklahoma factory prices also increased to the $700 mark by the end of last month with offers framed from $650-$700/t ex-works (EXW -- a shipping arrangement in which a seller makes a product available at a specific location, but the buyer must pay the transport costs) in the region based on tight availability, up from $475-$500/t EXW in late August.

Transportation lines in the U.S. remained constrained in September due to low water in the Mississippi River, as well as short supplies of rail cars and truck availability. Tight supplies as well as expectations for a good fall application period show a firmer picture for U.S. ammonia prices in the short term.

International: The global ammonia market firmed through September as competition for prompt tons intensified.

In Asia, prices climbed on news that the restart of operations at Ma'aden's 1.089 million metric ton (mmt) MPC ammonia plant in Saudi Arabia would be further delayed after earlier expectations to resume production mid-September following extended downtime.

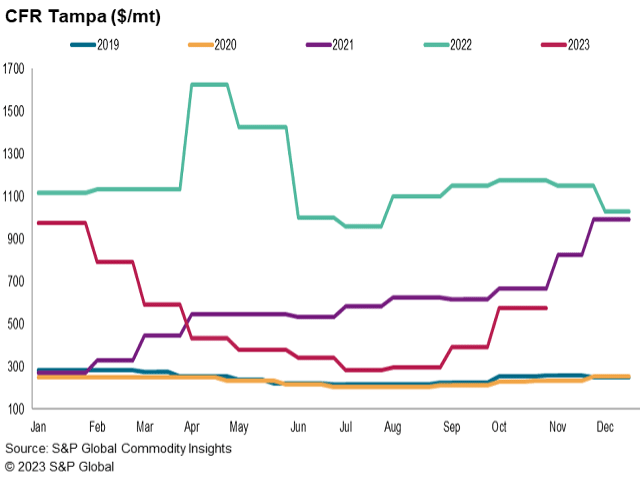

The west also felt the stress of ammonia supply constraints. In late September, Yara and Mosaic agreed on a monthly contract price at Tampa of $575 per metric ton (mt), cost and freight, (CFR -- sales price with delivery costs included) for October deliveries -- a significant increase on the $390/mt CFR agreed by the parties for September. The higher settlement followed a flurry of spot deals, including a 15,000-mt purchase from Trinidad by Nutrien for late September/early October delivery at $580/mt CFR Geismar.

Ammonia prices in the Caribbean followed Tampa higher to $520-$530/mt Caribbean FOB in the wake of the higher settlement price. Spot prices in the Black Sea rose similarly to $565-$570/mt FOB, higher than $315-$320/mt in the previous month on a nominal basis.

The short-term outlook for global ammonia prices is firm.

UREA

Domestic: Talk of a new Indian tender continued to circulate in the market following the conclusion of the previous India tender, which contributed to less liquidity as well as lower landed prices for barge sales at the end of September.

NOLA urea barges ended last month from $370-$418/t FOB, higher than our assessment of $340-$376/t FOB in the last week of August. September barges continued to trade toward the higher end of our assessments during the month while October trade tended to compose the lower end of our range.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

River terminal offers were stable from August at $450-$475/t FOB as interior markets awaited further direction from the NOLA market in the absence of much domestic demand last month, which tended to drift during lulls between news about India's purchasing.

Fertilizer barge loading drafts were reduced anywhere from 15%-28% for dry bulk along the Mississippi River due to the low waters, according to American Commercial Barge Line, with tow sizes also reduced. Grounded barges caused further delays in shipping throughout the river system last month.

International: India dominated the global urea market headlines last month with its Sept. 15 tender and expectations of another tender to follow. While prices against the tender were at least $20/mt lower than expected, sentiment improved as India failed to buy enough tons for its requirements, paving the way for additional purchase tenders before 2024.

Urea prices in Egypt last month rose to $420/mt FOB, up from $380-$400/mt FOB in late August with the modest price increase reflecting lower-than-expected price levels in India despite good demand expected until the end of 2023.

Spot prices in Brazil climbed higher last month in a market where sanctioned products from Venezuela and Iran competed for market share, capping higher potential price increases. Market prices were assessed at $390-$405/mt CFR at the end of September compared to $345-$350/mt CFR in late August.

Market players estimated India needs around 3 mmt of urea by January, which could result in several quick-fire tenders in the final quarter of 2023. If fresh Indian buying of over 1 mmt coincides with Brazil, Latin America, U.S. and Europe stepping in, we could see values head higher. If not, urea could remain soft.

UREA AMMONIUM NITRATE (UAN):

U.S. UAN markets were mostly quiet through September. Sellers in North America were said to have taken comfortable orders ahead of the fall period, leaving relatively fewer volumes available to offer in the spot market. Volatile movements in urea prices also kept those in the nitrates market wary of any large shifts to come, leading many to wait for further direction before stepping back into the market.

NOLA UAN barge markets were assessed at $240-$260/t FOB, higher from the $220-$230/t FOB range at the end of August. As mentioned above, tighter availability was the primary reason for offer levels moving higher last month.

Major terminals along the Mississippi River also increased by a similar amount to $275-$290/t FOB for UAN 32%N with Cincinnati at the high end and St. Louis on the low. This is a month-over-month increase from end-August price levels of $255-$260/t FOB.

UAN offers on production in eastern Oklahoma ranged from $265-$275/t EXW to end September, up from $240-$245/t EXW in late August. Sellers, however, were reported to be few as some producers in the area had pulled offers earlier in the month and had yet to return to the market.

Nitrates prices looked poised to remain stable to stronger for the remainder of 2023.

PHOSPHATES

Domestic: Phosphate prices continued to firm in the U.S. last month as higher inventories leading into 2023 were cleared by a strong spring application period, leaving the country with relatively few stocks in comparison to another strong demand period expected this fall.

NOLA DAP ended September assessed at $540-$545/t FOB, approximately $20/t higher compared to DAP barge prices at the end of August. MAP barges increased similarly to $635-$650/t FOB compared to the last assessment of August of $630.

River terminal MAP prices proportionally increased to $690-$710/t FOB, higher from end-August levels of $675-$695/t. DAP price levels, meanwhile, did not see as much spillover support from NOLA (New Orleans, Louisiana) compared to DAP and were assessed mostly flat month-over-month at $580-$595/st FOB DAP.

Last month, the U.S. Court of International Trade decided to order the U.S. International Trade Commission (ITC) to re-evaluate its duties on Moroccan-origin phosphates.

The OCP Group welcomed the Sept. 14 decision by the court on its appeal challenging the countervailing duty of 19.97% imposed by the Department of Commerce on imports of fertilizers from Morocco into the United States.

Neither the ITC nor the U.S. Department of Commerce have thus far changed anything from their earlier determinations, as Mosaic said in a press release commenting on the ruling from the court. As a result, countervailing duties on phosphate fertilizers currently remain in effect with no changes to the rates applied at the border.

International: Global purchase activity at the end of September was centered in Asia, particularly from buyers in India who showed no sign of slowing demand. As China headed off for its Golden Week holiday, activity from producers was subdued. However, producers were reported comfortable with existing commitments.

India was understood to have bought 60,000 mt DAP from Saudi Arabia at a higher $595/mt CFR for October loading, up from our end-August assessment of $550/mt CFR. There could be an increase in consumption during the Rabi (winter) season, and importers were expected to buy additional volumes in October after getting clarity on nutrient-based subsidy rates.

Our Brazil MAP price assessment increased to a similar but smaller degree from $530/mt CFR in early September to $550/mt CFR towards the end of the month against a backdrop of tight supply. Phosphate business was limited with some suppliers reported to only have product available for November arrival. Demand for safrinha was expected to pick up around this time, but many are taking a wait-and-see approach and keeping an eye on corn prices.

Our short-term outlook on global phosphate prices at the end of September was firm.

POTASH

NOLA granular potash barges ended September assessed at $345/t FOB, up from $325-$335/t FOB in August on stable fundamentals along with steady increases to offers on North American-origin products as well as import volumes on shorter availabilities.

Both phosphate and potash demand were beginning to ramp up alongside fall harvest efforts in the southern U.S. along with pockets of the west at the end of last month, but peak demand for the season was not expected to emerge until later in October.

River terminal potash prices were also stable in the meantime from August to September, with offer levels at primary trading hubs along the Mississippi ranging from $380-$395/t FOB.

While imports haven't lagged too heavily in 2023 compared to 2022 levels, market participants expect increasing demand may outpace available supplies during the fall fertilizer run to come.

With decreased barge transit capabilities due to low water, obstacles remain for Canadian supplies to be efficiently shipped into the U.S., alongside tight railcar and truck availability as well, leading us to take a more stable to firm expectation on U.S. potash prices to end 2023.

Editor's Note: This information was supplied courtesy of Fertecon, S&P Global Commodity Insights.

(c) Copyright 2023 DTN, LLC. All rights reserved.