DTN Fertilizer Outlook

Domestic Wholesale Fertilizer Prices Slide in March; Outlook for April Mixed

The following is a recap of fertilizer price trends and market developments for the month of March.

AMMONIA

Domestic: Following another reduction in the Tampa ammonia contract for April shipments last month, U.S. ammonia prices did not initially fall lower in the Corn Belt. However, the trend of softer nitrogen prices has been present in the market in 2023 so far and landed ammonia prices were said to be falling.

Ammonia in the Corn Belt was previously offered from $750 to $$840 per short ton (t) free-on-board (FOB -- or sales price per ton without additional transportation costs considered) earlier in the month. Although no changes were heard to posted offers, market participants confirmed it was a buyers' market to end April alongside expectations that cheaper deals could be struck.

In contrast, factory ammonia offers saw a fast reset in eastern Oklahoma, being offered around $500 to $525/t FOB, down from $550 to $570 FOB prior to the past day's Tampa settlement.

Retailers in March were still carrying a fair amount of length from late last year, and farmers were still being quoted the much higher retail value around that time of over $1,000 FOB. Once these carryover volumes have been cleared out, further price reductions are expected.

In the short term, we expect U.S. domestic ammonia prices to fall lower alongside the weaker Tampa, following sharp reductions in other U.S. nitrogen fertilizer prices in first-quarter 2023.

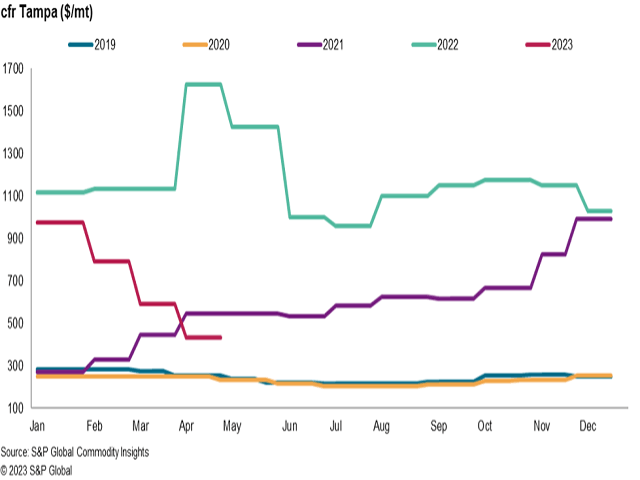

International: A major, long-awaited correction got underway in the ammonia market in March, due to the continued reduction of European natural gas prices, which brought down production costs in the region.

It was announced late February that Yara and Mosaic had settled at $590 metric ton (mt) cost-and-freight (CFR, or cost of sale per ton with shipment costs included) Tampa for March shipments.

Then, in late March, Yara and Mosaic had agreed a further price decrease of $155 mt, settling at $435 mt CFR Tampa for April deliveries. It was the lowest settlement at Tampa in more than two years, since February 2021, and followed first-quarter corrections that have, in total, more than halved the value of ammonia in the U.S. Gulf since the start of the year.

The latest settlements at Tampa, and their impact on Caribbean pricing, were also felt in the Black and Baltic Sea regions, which were assessed at $380 to $400 mt FOB and $340 to $360 FOB, respectively. This is down sharply from February prices, which were assessed from $625 Black Sea and $585 Baltic.

Ammonia market participants noted May could bring another sharp reduction in the Tampa contract, potentially falling into the mid-$300s CFR given current market conditions. The price outlook for the global ammonia market in the short term is weak across both the Western as well as Asian markets.

UREA

Domestic: Nitrogen fertilizer pricing overall continued to fall in the U.S. through March, and urea was no exception, sinking lower following the conclusion of another disappointing India tender last month.

Urea barges at the trading hub in New Orleans (NOLA) ended March trading from $290 to $315 t FOB, lower from the last week of February at $310 to $335 and the first time for urea barges to trade below $300 since early 2021.

March terminal urea offers on the Mississippi River were heard in line with NOLA barges at $370 to $410 t FOB at hub markets including St. Louis, Tulsa, and Cincinnati -- up from the previous month's range of $355 to $390. In Oklahoma, a combination of rapidly increasing demand as well as slower shipments due to high water on the Arkansas River supported higher pricing in the area compared to the typical spread between Tulsa and other terminals.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

Demand remained virtually nonexistent until the earlier-than-average opening of the Upper Mississippi River showed spring applications were just around the corner. But prices did not really take off until early April.

With spring demand having since then taken off on most fertilizers, urea prices seem supported in the short term as product runs thin in some places. Some pressure may be more apparent in May, as the recent spike in urea prices led to several more cargoes booked from the likes of Russia, Nigeria and the Middle East.

International: Global urea markets continued their roughly six-month downward trajectory in March with weak demand coupled with oversupply.

The results of India's March 3 tender were the focus of the first half of the month, with prices over $240 mt lower than a previous tender in November. The buyer ended up accepting 1.1 mmt, and world pricing fell on the following trades with excess product looking for homes.

Egyptian urea prices dropped lower to $335 to $345 mt FOB by the end of March, down from $380 to $395 in February on account of the oversupply of product left on the table by India. Brazilian landed sales fell by a similar amount to $310 to $315/mt CFR as the country had little appetite for exporter's urea last month in their off season.

Buyers held the upper hand throughout the month, with spotty demand from India, the Americas and Europe pushing prices downward. The Indian government further revealed there were adequate stocks already for Kharif season and it appeared that market may be covered for longer than initially thought.

The outlook for world urea prices was weaker on less-than-expected spring planting in India and lingering oversupply in most key regions. More downward pressure is expected on pricing, but the U.S. has provided a bit of hope in April's burst of spring activity so far.

UREA AMMONIUM NITRATE (UAN)

Price movement for UAN was mixed in March between areas of high and low demand in the emerging spring observed at the time.

UAN barges at NOLA ended last month priced from $270 to $280 t FOB, $10 lower from barge sales in February. Prices appear supported elsewhere in the country, however, with buyers who were searching for product more eager to get more promptly available tons positioned upriver.

River terminals on the following trades ranged from $325 to $330 t FOB in March along the Ohio River, and slightly lower at other terminals as low as $320 -- still higher from the range of $300 to $310 on offer for UAN 32%N at main hub terminals in February.

The East Coast had yet to hit its stride in March, as well, with import cargo pricing in the region flat from prior-month levels at $400 to $420 mt CFR and $320 to $330 t ex-tank. Freight rates between the U.S. and Russia remained at elevated levels last month, further discouraging additional export sales.

Aside from the higher pricing along the Mississippi River, most other U.S. markets saw little activity in March. Eastern Oklahoma production sites, however, did see some greater demand in the local area and ended March at $290 to $295 t FOB ex-plant, up from discounts offered earlier in March as low as $255 to $270 before prices were posted back higher.

Nitrate pricing in the U.S. is expected to begin climbing later in April, with more of the main growing areas due to get sidedress and top-dress underway in the coming weeks.

PHOSPHATES

Domestic: The narrative in the U.S. phosphate market in March revolved around a positive expectation for the preplant application season, but demand remained somewhat slow and steady in the meantime with prices supported as buyers snatched up cheaper import volumes on offer.

DAP barges at NOLA were assessed $600 to $610 t FOB, slightly higher versus our end-February assessment at a flat $600. MAP barges similarly sold higher to $575 t FOB market in March, up from the $565 to $570 traded in the prior month.

With Southern river terminal demand eventually picking up and the market feeling the strain of lagging supplies, phosphate prices rose to $655 to $695 t FOB for DAP, up from $655 to $665 t in February. MAP prices, meanwhile, remained mostly flat around $625 to $645 t FOB on account of the Northern states still weeks away from their own spring rush.

Terminal pricing moved higher accordingly in Inola, Oklahoma, where DAP at the end of March fetched a $20 t premium over offers in St. Louis, attributed to the increasing demand as well as a slower rate of resupply barges to Oklahoma.

Earlier this year, action from the U.S. Department of Commerce included lowering the import duty for Russian phosphates, and in the most extreme case, cutting EuroChem's production-subsidy rate nearly in half. Fertecon observed an uptick in Russian phosphate imports following the decision.

We expect phosphate prices to remain supported in the short term, as the product has become extremely tight during its peak usage time.

International: International phosphate values dropped throughout March against a backdrop of sliding raw material costs.

Peak shipment demand in Western Europe and the U.S. at the time were seasonally slow, and with key Asian and Latin American buyers of India, Pakistan, Bangladesh, Brazil and Argentina in no urgent need of material, a large demand gap remained to be bridged, and producers were cutting asking prices by the day in an effort to drum-up fresh interest.

For example, Indian DAP prices dropped to $578 mt CFR in March from as high as $640 to $643 in February. Buyers were reluctant to step back into the market ahead of an expected adjustment to the government's fertilizer subsidy program.

MAP in Brazil fell similarly to $600 to $620 mt CFR, down from $650 to $660 in February in what was already a soft market, which remained dormant through the month.

With demand for phosphates lackluster in major buying countries and with no change in sight, our short-term price outlook for the global phosphates market remains weak.

POTASH

Sentiment for potash prices improved overall in March, following the climbing demand for phosphates, which would typically also be a boon for potash.

2022 was a poor year for potash demand, and market participants were expecting 2023 to be a better year by comparison at the very least. More positive weather conditions emerging have reinforced this belief, as potash volumes have similarly drained and are becoming less and less available.

Potash barges at NOLA traded from $370 $378 t FOB in March, mostly unchanged from the $375 assessed at the end of February. Import product was previously offered at $365 FOB NOLA earlier in March, but reported sales climbed as North American producers were able to achieve higher barges sales as cheaper imports were depleted.

In contrast to barge prices, Mississippi River terminal prices fell lower in March. The last week of the month saw prices ranging from $415 to $435 t FOB at major terminals in St. Louis and Inola, Oklahoma, having fallen from previous offers from $440 to $460 in February as the more positive demand sellers were expecting did not emerge until April.

The early departure of barges northbound on the Upper Mississippi River was a good first sign for potash demand, and a sluggish pace of imports contributed to the supply squeeze we are expecting to emerge similar to phosphates.

In the short term, we expect U.S. potash prices to firm through April, with potential for prices to remain elevated if the supply scenario does not improve later this year.

**

Editor's Note: This information was supplied courtesy of Fertecon, S&P Global Commodity Insights.

(c) Copyright 2023 DTN, LLC. All rights reserved.