Todd's Take

Apparently, Yes, Some Think Corn Farmers Should Be Harshly Penalized

On Tuesday, March 19, my co-workers said some people on social media were upset about the March 18 Todd's Take (https://www.dtnpf.com/…). To be honest, I didn't understand what was so controversial. Some postings were complimentary, and the only email I got thanked me for the article. Some of the social media comments were emotional, however, and didn't explain what they were so upset about. Here is one of the more specific comments that may help the conversation.

One said, "Same thinking should apply to short crops. See how that goes over."

The response to that is simple. If there is one market incentive in corn that works, it is that farmers have incentive to plant and maximize crop yields every year. Since 1980, I count six short corn crops, and the short supply of corn never lasted very long. For preventing famine, I think we can agree the market has one incentive that works. The problem, of course, is that is only one side of the market.

To highlight how defenseless the corn market is during times of plenty, consider this simple comparison of USDA's average farm prices for corn and USDA's national cost of production estimates. For the 43 seasons between 1980-81 to 2022-23, the average farm price for corn has exceeded USDA's cost estimate 15 times. If we limit the comparison to the seasons before ethanol arrived, there were four seasons in 26 that showed a profitable average farm price. That is not just a streak of bad luck. That is a market with bad incentives. It is also why I contend biofuels are the best practical hope for restoring profitability in ag and am eagerly waiting for the announcement of Sustainable Aviation Fuel (SAF) requirements.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

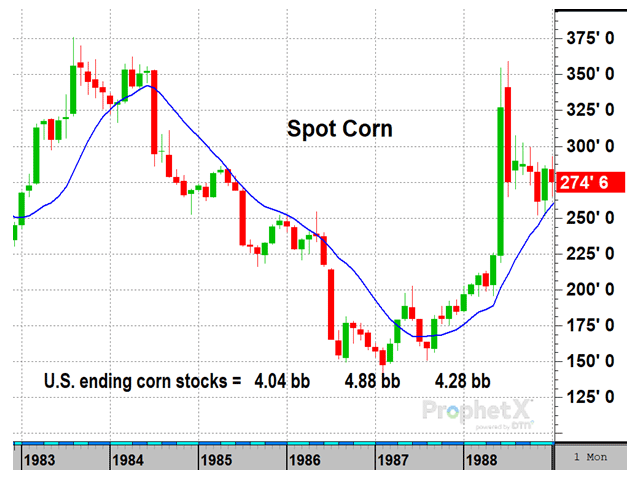

Diving a little deeper, if we look at corn's unprofitable years, we see three long stretches. An 11-year stretch of losses from 1983-84 to 1993-94, a 10-year stretch from 1996-97 to 2005-06 and a six-year stretch from 2014-15 to 2019-20. I started my career witnessing a mildly unprofitable season of 1984-85 turn into a 4.040-billion-bushel (bb) corn surplus the following year, followed by a 4.882-bb surplus, followed by a 4.259-bb surplus. Where was the market mechanism at work to restore prices and supplies to their magical equilibrium levels those three years? There wasn't one.

It took the drought of 1988 to bring the surplus down. Yes, there were chances for higher selling prices in 1988, but even the drought did not put the average farm price above the production cost that season.

Given the bearish skew of market incentives in agriculture, some are outwardly upset by the amount of money the government has handed out over the years, dealing with various disasters and trying to keep farmers in business through difficult market challenges. As one comment on social media put it, "Did he forget about 2018-2023 ... the regular taxpayer subsidies and then billions of lard ..."

Here is how I see it. As a nation of 336 million people and growing, we actually need the 3.46 million producers USDA says we still have. They're not selling us cryptocurrencies; they're producing the food and feed and some of the fuel we all need. Instead of leaving farmers trapped in a market that is prone to long-term surplus and then trying to keep them afloat with government checks, it seems more constructive to start having conversations about how to introduce incentives into the marketplace that prevent long-term surplus and give farmers better chances at profitable prices.

In today's market, being included in the mix of feedstocks eligible for SAF is the best hope agriculture has for creating a more profitable future, and I certainly hope corn-based ethanol and renewable diesel will be accepted. Apart from that political decision, farmers who don't own their own ground or aren't blessed with the highest-yielding soils are going to continue to have a tough road.

For those who think the current system is fine, I wish you well, but respectfully disagree.

**

The comments above are for educational purposes only and are not meant as specific trade recommendations. The buying and selling of grain or grain futures or options involve substantial risk and are not suitable for everyone.

Todd Hultman can be reached at Todd.Hultman@dtn.com

(c) Copyright 2024 DTN, LLC. All rights reserved.