USDA Reports Review

Few Surprises in March WASDE; Corn Falls on Reduced Exports

The March 2023 World Agricultural Supply and Demand Estimate (WASDE) report had few major surprises, with the primary focus before the report on U.S. corn exports and on Argentine corn and soybean production. While the Argentine changes were larger than the trade had expected, it was more in line with private estimates. However, the U.S. corn market took the news of lower exports hard, falling sharply.

CORN

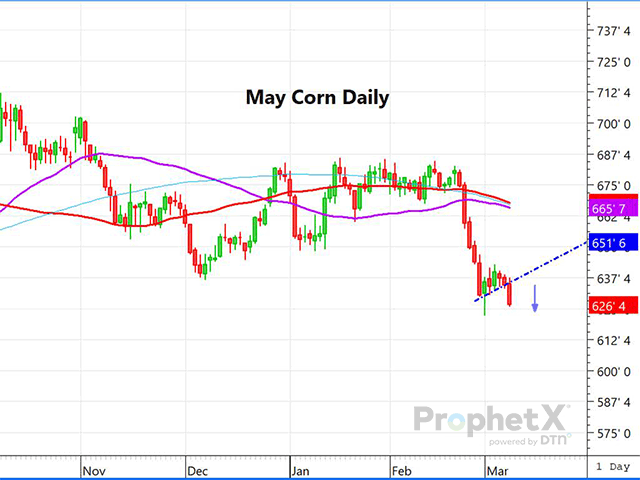

Going into the March WASDE, the only change expected domestically for corn was a reduction in export sales and rise in ending stocks to account for the slow pace of export sales and inspections. That's just what we got, but the export drop was more than expected at 75 million bushels (mb), raising the ending stocks by a like amount to 1.342 billion bushels (bb). That was about 43 mb higher than what Dow Jones' pre-report survey had as an estimate. Corn's average price for the year was reduced by a dime to $6.60 per bushel.

On the world side, traders were highly focused on changes to Argentine corn and soybean production. Argentine corn production was pegged at 40 million metric tons (mmt), compared to the average trade estimate of 43.2 mmt (1.7 bb) and last month's 47 mmt (1.85 bb) estimate. Perhaps the reason why this was not as bullish as it could have or should have been is that traders were aware that private analyst estimates suggested USDA may have been overestimating Argentina's production all along. In addition to the Argentine production decline, Argentine exports were lowered by the same amount to 28 mmt (1.1 bb). World ending stocks of corn rose 1.2 mmt to 296.5 mmt (11.67 bb), compared to trade expectations for a decline of 1.4 mmt from February. Trading near unchanged prior to the report release, the U.S. and world changes weighed on spot May and new-crop December futures by the end of the day, both plunging close to 9 cents.

SOYBEANS

Ahead of the report, there were few changes expected for soybeans in the U.S. balance sheet, and once again, the primary focus seemed to be on South American changes. A modest surprise did occur on the domestic side when U.S. soy exports were increased by 25 mb to 2.015 bb to account for the faster shipping pace and lower Argentine production. To offset some of that, domestic crush was dropped by 10 mb to 2.220 bb, resulting in only a modest 15-mb decline in ending stocks -- a still very tight carryout and the lowest in seven years. Soybean average price was left untouched at $14.30 per bushel. U.S. soybean oil exports were dropped by 200 million pounds to just 500 million, as domestic use for biodiesel appears to be the focus. Soybean oil prices dropped 2 cents to 66 cents, while the average soymeal price rose by $15 per short ton to $465.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

With the Dow Jones trader survey looking for a drop of 4.7 mmt on Argentine soy production, USDA chose to move closer to private estimates, slashing production by 8 mmt (293 mb) to just 33 mmt (1.21 bb). This may still be 3 mmt to 4 mmt (147 mb) higher than some analysts are looking for -- perhaps reason enough for the lack of bullish enthusiasm that resulted. That, in addition to Brazil's record crop that is already near 50% harvested, seems to have weighed on the market, as soybeans rose only modestly on the bullish news. World ending soy stocks fell to just 100 mmt (3.67 bb).

Changes in Argentine soymeal production saw a decline to 27.5 mmt from 29.09 mmt previously, and exports of meal were lowered to 24.9 mmt from 26.2 mmt. Soybean oil production declined to 20.57 mmt from 20.97 mmt previously, while exports fell from 5.10 mmt to 4.75 mmt. Argentine soy imports were raised by 1 mmt to 7.25 mmt (266 mb), while Argentine soy exports fell by the same decline in production -- 7 mmt to 28 mmt (1.03 bb).

May soybeans were trading up 9 cents prior to the report but could only muster a 2 1/4-cent higher finish, with meal lower and bean oil higher.

WHEAT

The wheat portion of the March WASDE report was kind of boring on the domestic front, with the U.S. balance sheet left totally untouched, with no by-class changes either. Dow Jones traders had looked for a small bump in U.S. ending stocks, but those were left unchanged at 568 mb.

On the world side, USDA chose to leave their lowball estimate of Russian wheat at 92 mmt (3.38 bb), despite private analysts looking at a crop of 100 mmt (3.67 bb). The wheat production estimates for both India and Australia were both increased by 1 mmt each, while Australia's exports were raised by 500,000 mt. Perhaps the largest surprise was the increase in Kazakhstan's wheat crop by 2.4 mmt to 16.4 mmt (602 mb). There were other minor changes, with an increase of 400,000 mt in Argentine production. World ending wheat stocks fell to just 267.2 mmt (9.82 bb) and the lowest since 2016-17. The reduction was largely due to lower stocks in China, as the previous year's demand was raised by 4 mmt (146 mb). Ending stocks figured down 2.1 mmt (77 mb) from February, and 2.7 mmt lower than trade expectations, but that failed to rally wheat.

FINAL THOUGHTS

The 2023 March WASDE was not a huge market-mover, although it did offer a few surprises. The larger-than-expected cuts in Argentine corn and soy crops had a muted impact, while corn futures reacted much more bearishly to a larger-than-expected decrease in U.S. exports. Should Argentine crops continue to move down more toward private estimates, there is little likelihood that U.S. corn exports will fall much more. Currently, record-large Brazilian crops expected have more than offset much of the Argentine loss, but the jury may still be out on the final Argentine numbers and the price impact that may have.

Dana Mantini can be reached at dana.mantini@dtn.com

Follow him on Twitter @mantini_r

(c) Copyright 2023 DTN, LLC. All rights reserved.