by

Alan Brugler

,

DTN Contributing Analyst

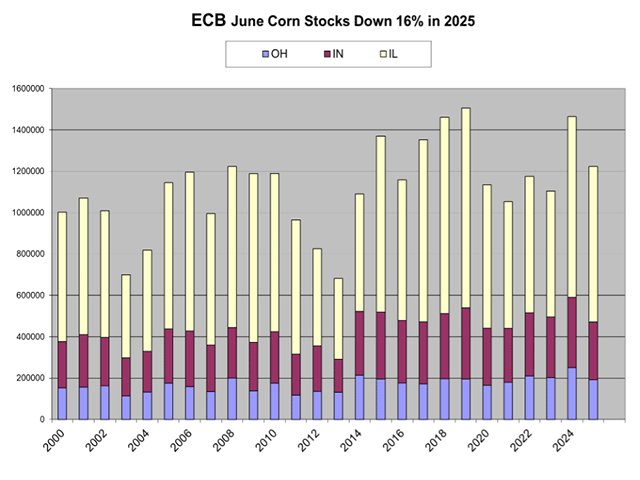

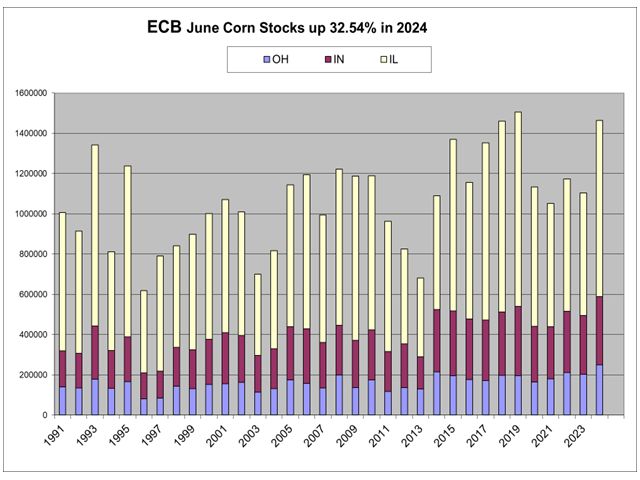

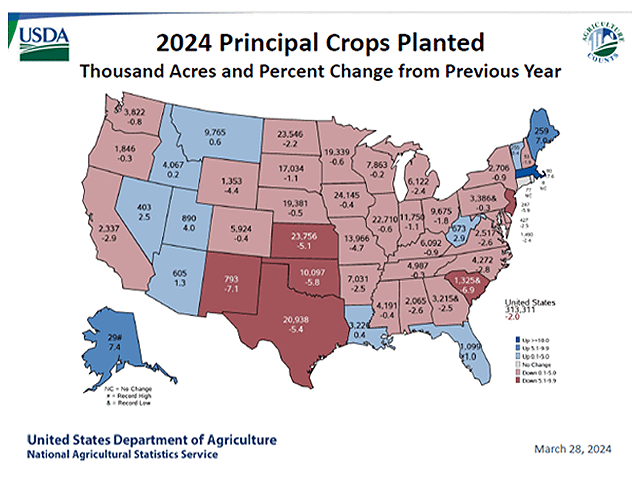

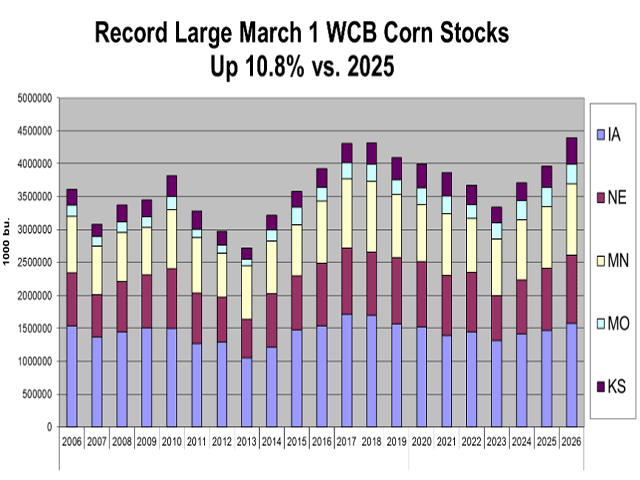

USDA's March 31 reports showed lower corn and wheat planting intentions, higher soybean acres, and mixed grain stocks, but tariff uncertainty, fertilizer costs, and ample supplies leave the 2026 crop outlook murky.