Fundamentally Speaking

Corn Farmer Marketing Patterns

U.S. corn farmers supposedly have been refraining from selling their recently harvested 2018 bushels on the market, deterred by low prices and having a little more storage space than they had expected given the drawn out harvest due to a wet fall in the Midwest that eliminated to a large extent any forced sales.

These producers, as opposed to soybean farmers, have not benefited from the Market Facilitation Program (MFP) which provides partial compensation to farmers and share-rent landowners for losses occurring because of trade disputes.

Soybean producers will get $1.65 per bushel while corn farmers will only receive a mere one cent per bushel, so they are much more dependent on some sort of recovery in market prices over the ensuing months.

P[L1] D[0x0] M[300x250] OOP[F] ADUNIT[] T[]

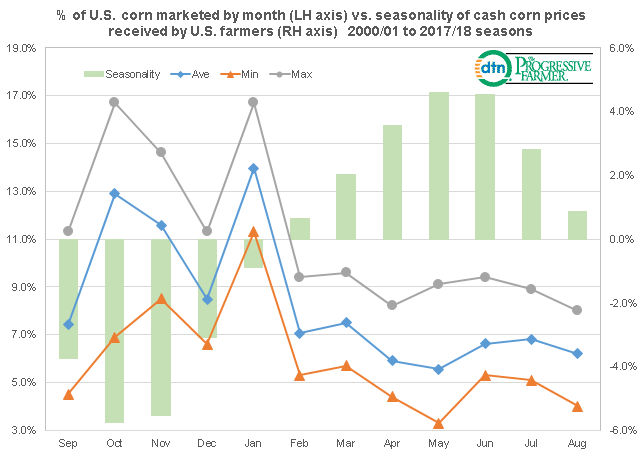

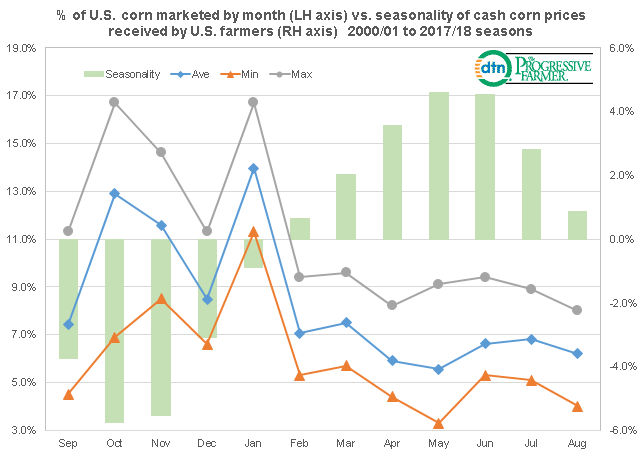

This graphic shows the percent of U.S. corn marketed by month during the marketing year that goes from September 1 to August 31 on the left hand axis vs. the seasonality of cash corn prices received by U.S. farmers on the right hand axis using data from the 2000/01 to 2017/18 seasons.

Even though farmers know that the lowest prices are usually at harvest, often when they have filled up their on farm storage they will sell some cash grain when supplies are heaviest to avoid making ground piles.

Thus, October is the second highest month for marketings at an average of 12.9% and for the past 18 years about 40.4% has been marketed by the end of the calendar year.

The most popular month for farmers to sell is January where the 2000-2017 average is 14.0% of their supplies marketed that month.

Reasons for this include some sort of post-harvest price recovery and producer desires to limit sales until after the first of the year for tax purposes.

We were curious to see how farmer marketings matched up vs. the usual season price patterns of corn where values are lowest during the harvest period and gradually improve from that point on with the higher prices seen in May and June that are respectively 4.6% and 4.5% above the yearly average.

Note that the 40.4% marketed from September to December does coincide with the lowest prices of the year as cash flow considerations and the need to generate funds for spring plantings often does not allow a producer to sell later in the marketing season when prices are higher, though utilizing forward contracts that do capture some of the carry in the market does enhance returns.

(KLM)

© Copyright 2018 DTN/The Progressive Farmer. All rights reserved.

Comments

To comment, please Log In or Join our Community .